The Two Weeks That Will Be

1. The UK

With UK headline inflation due to head back to the Bank of England’s target for the first time in three years on Wednesday, Rishi Sunak would have been hoping for a vote of thanks from the Great British Public. Instead, postal votes will be landing on people’s doorsteps just as Sunak’s net approval rating has fallen to its joint lowest level and the opinion polls have seen Reform UK move ahead of the Conservatives for the first time.

Nigel Farage is now able to suck up oxygen from the campaign, penning a rebuttal in The Telegraph to David Cameron’s interview in the Times, where the latter called the former ‘incredibly divisive’, which then led Nigel to call David ‘a disgrace to Britain’. As this exchange demonstrates, once you make a campaign about your opposition, you give them the momentum (cf. Hilary v Donald, 2016). But this campaign isn’t over after July 4th – this is a battle for the heart of the Conservative Party.

Not that financial markets should pay much attention to that. The Labour Party are forming the next government, barring any astonishing mistakes. Even the supposed 17 tax rises that Labour have not ruled out, according to the Conservatives, raises no fear. It’s just assumed that they’re coming, and/or that a stable government for the first time in years can deliver its own growth dividend. This is the heart of Rachel Reeves’ “Securonomics” plan: a strategic state can work with private investment to get growth going.

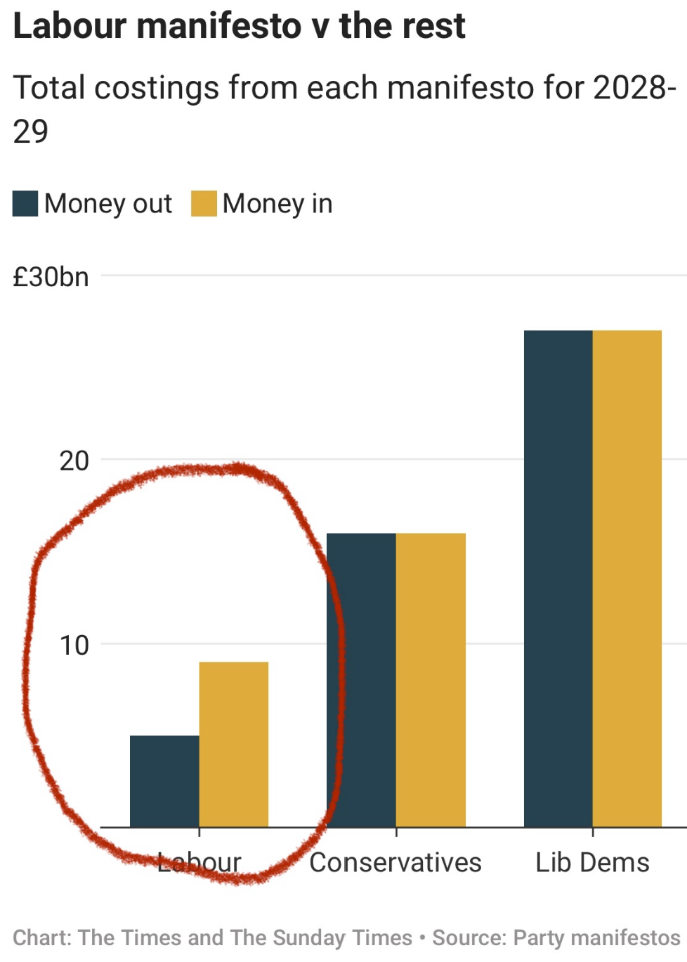

Despite the length of the Labour manifesto (142 pages) the scale of its plans were far smaller than those of the Tories and the Liberal Democrats:

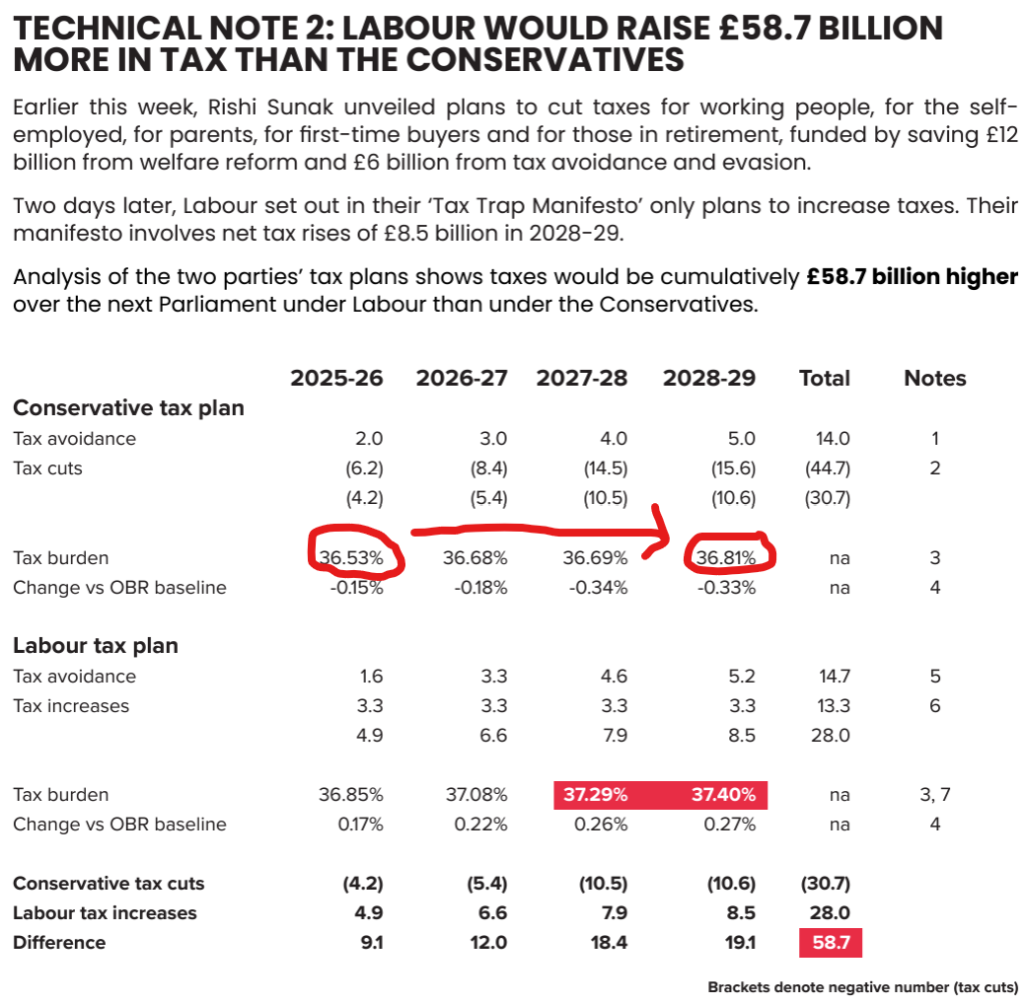

This will not stop the Conservatives from “Project Fear Keir“. Don’t give him a big majority, don’t give him a blank cheque to raise taxes, don’t let him compromise national security, etc. The trouble is, the Conservatives got a big majority and then proceeded to raise taxes, preside over increases in illegal immigration and churn through three Prime Ministers. Even the document that proudly trumpets the huge tax burden under Labour’s manifesto also shows that it would rise under the Conservatives’ plans:

Focusing on the first decimal place is classic Sunak Spreadsheetism. Keir Starmer wants to talk about the bigger picture. “I have three priorities for our economy: growth, growth, growth. For too long, our economy has not grown as strongly as it should have done” said… Liz Truss in October 2022. Keir Starmer has just said “I utterly reject the proposition that we cannot do better than we’ve done in the last 14 years… We’re going for growth. Our manifesto is for growth, it’s a plan for growth. That has been the missing ingredient for 14 years. We intend to turn that around“.

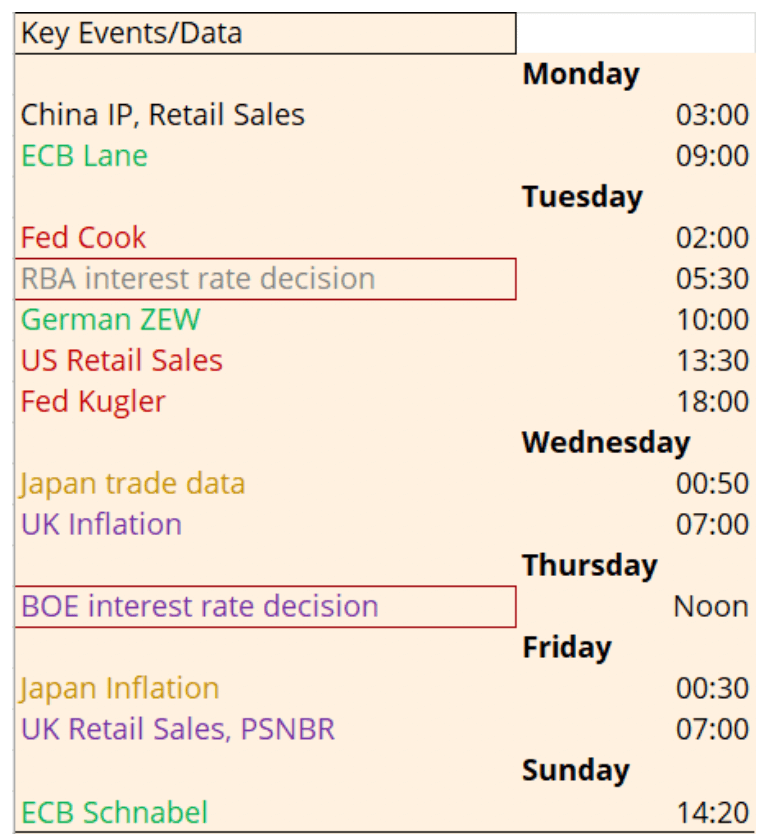

On Friday we will get an indicator of the scale of the problem, with the latest UK Retail Sales and Budget Deficit data. The Bank of England on Thursday won’t be in any rush to cut rates to boost growth. They had already cancelled all speeches over the election period and there’s no monetary policy report or press conference. They are unlikely to want to make any changes at their next meeting given they will want to see how Labour’s fiscal policy pans out in practice, not to mention how services inflation remains stuck around 6%. The Financial Stability Report on Thursday 27th June is also likely to take a wait-and-see approach, not least because the System-Wide Exploratory Scenario exercise won’t be concluded until the end of the year. The Bank of England are happy to hang out in the background, for now.

2. The RBA

The BOE can use the time to adopt an RBA approach. Interest rate cuts have continued to be priced out of the curve after inflation failed to moderate as much as expected. Growth is softening but employment data has improved. There had been some rumblings that the next move might even be a rate hike. But the RBA have remained on hold and will do so again on Tuesday as “high for longer” becomes the new “rate hike”.

Having missed the move higher in inflation, central banks don’t want to get it wrong again. Hence Fed officials now forecast a marginal reacceleration in inflation towards the end of this year and the dot plots have moved up concomitantly. The Fed’s Cook and Kugler can clarify their opinions further when each speaks on Tuesday.

3. France

The first round of Macron’s surprise Legislative Elections takes place on Sunday 30th June. Two weeks after that we will know if his gamble has paid off. But what is his game? His party are floundering in the polls and lost almost half their seats in the European Parliament elections while Marine Le Pen’s National Rally surged into top spot with 32% of the vote, double that for Macron’s group.

But legislative elections for France itself are another matter, where turnout will rise. By calling a snap election he has certainly exposed the fissures on both the left and the right. With such a short deadline to announce alliances and candidates, there have been chaotic scenes.

- The President of the Republican Party announced they should seek an electoral alliance with Le Pen; other senior officials disagreed; he barricaded himself into their headquarters until someone found a spare set of keys; he was then expelled from the party; which was then overturned by a Parisian court.

- Four of the five newly-elected MEPs from the far right Reconquête Party then went against the party’s founder Eric Zemmour, including Marion Maréchal (niece of Marine Le Pen), for failing to ally with National Rally; National Rally said they didn’t want to be associated with Zemmour; and then Zemmour promptly fired Maréchal for her “betrayal”.

- The four main left-wing parties have formed the “New Popular Front” but it’s not entirely clear who will lead it; the leader of the Socialists, Raphaël Glucksmann, has had to break bread with firebrand quasi-communist Jean-Luc Mélenchon with whom he has previously argued over matters such as Gaza; Glucksmann acknowledged his voters in the European elections “may feel betrayed”; Mélenchon has already removed some of the moderates from his party’s candidates list for not supporting his policies.

- Former President Francois Hollande has even thrown his hat into the ring, announcing he would stand for the NPF as “I just want to be of service”; however a senior party official said they were “devastated” by his return.

Macron kicked off the campaign by criticizing both blocs as “unnatural alliances” and calling on “men and women of goodwill who are able to say ‘no’ to extremes on the left and the right to join together to be able to build a joint project“.

But each side is currently polling higher than his own. The latest poll showed the National Rally could win 195-245 seats, the New Popular Front 190-235 and Macron’s alliance only on 100. With 577 seats in the National Assembly that would leave nobody with an overall majority.

This was already the case following the last legislative elections and Macron was already struggling to get anything done. He had to bypass parliament with constitutional weaponry, activating Article 49.3 many more times than any of his predecessors. France’s President is constitutionally the most powerful executive position of any western democracy and Macron only has three years left in position before his term must end. He will still only be 49 by then and presumably has an eye on his legacy. Why let it be ruined by encouraging tumult and friction with his legislative branch of government?

A political type has suggested to us that it is better to hunt than to be chased. Macron was already up against it. A snap election crystallises the choices of left, right, or centre. He hopes to peel off voters from the extremes and bring them back towards him. The French electoral system only allows two candidates to go into a run-off in the second round. It’s a least ugly contest. Macron hopes that this will force those against the other extreme to hold their nose and back his centrist alliance. If voters are split three ways then that should mean two-thirds don’t want the other side to win.

But his candidates have to get into the final round to be in with a chance. If more voters sit on left or right than in the centre, his candidates won’t even make it.

We will see in real time the fragmentation of the electorate that has been taking place across the world over the last 15 years. It started with the banking crisis splitting voters into those for and against the establishment. Then the pandemic and inflation divided people further into those who want intervention from the state versus those who don’t. Emmanuel Macron benefited superbly from the first split. He managed to succeed as an insurgent when the old political parties were felt to have failed, bursting onto the scene with a whole new movement. Now, having ruled over an exceptionally volatile period where people were locked up and then, thanks to inflation, became poorer, he hopes that their answer will be that they want more of the same. Or at least that they don’t want to take a risk with unproven populist firebrands.

We think this is mistaken. Macron might have been encouraged by the success of Pedro Sanchez in Spain who last summer called a snap election when he was up against it and managed to remain in power even though his party was eclipsed by a rise for the centre-right opposition party. Time has moved on since then and the right and left wings of French politics have been steadily growing their power base for several decades. The right wing Vox party in Spain is barely a decade old whereas the Le Pen family have been contesting at the highest level ever since Jean-Marie made his shock appearance on the second round presidential ballot in 2002.

Nor is Marine Le Pen another Georgia Meloni, talking tough but playing nice. Marine might have detoxified the party and moved on from Frexit but she is still committed to changing the way the EU operates and has an unsettlingly close relationship with Putin.

All of this means that there should be a significantly higher risk premium on French – and ultimately Eurozone – assets. This is the beginning of political volatility across the continent, not the end.