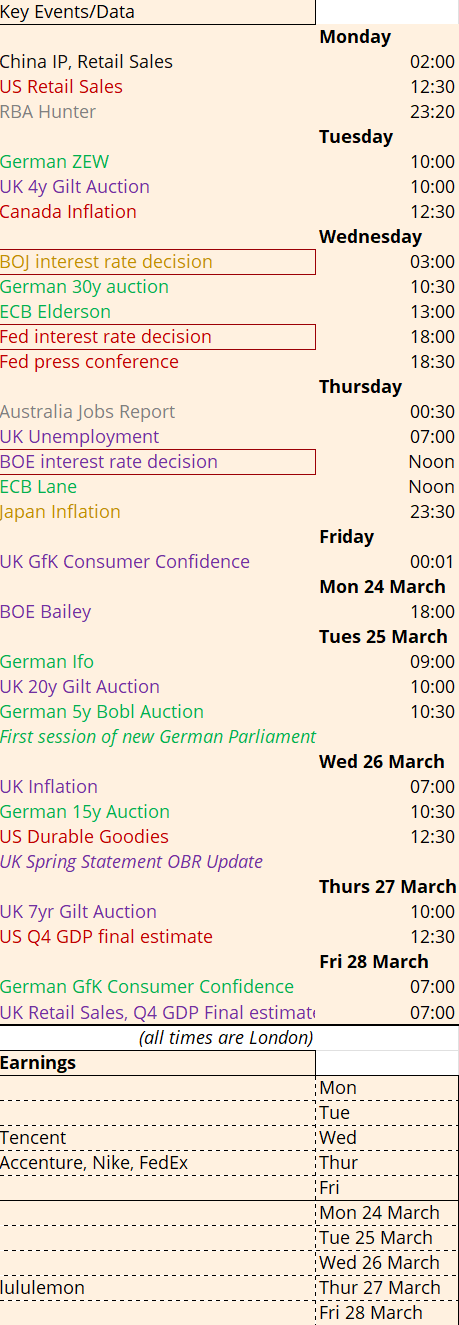

The Two Weeks That Will Be (16th March 2025)

1. Trump

“the United States will impose a 5% Tariff on all goods coming into our Country from Mexico, until such time as illegal migrants coming through Mexico, and into our Country, STOP. The Tariff will gradually increase until the Illegal Immigration problem is remedied”. So tweeted Trump, on the same day that his Vice President flew back from Ottawa after seeing Trudeau and when the White House took a procedural step to allow it to submit a US/Canada/Mexico trade deal to Congress. The year, of course, is 2019. Specifically, 20th May 2019, when Trump lifted steel and aluminium tariffs on Mexico, only to issue his fresh tariff tweet 10 days later, and then to rescind the threat 8 days after that. And all of this six months after the leaders of the US, Mexico and Canada had signed the text of the USMCA trade treaty at the 2018 G20 Summit in Argentina.

So, Trump slapping on tariffs, threatening to ratchet them up, signing deals, and rescinding tariffs within a relatively short space of time is nothing new. Back then, the news took the VIX up, although nothing like the spikes seen in the “Vol-mageddon” of 5th February 2018 or the fear of a tighter Fed in December 2018:

The S&P500 did fall just over 7% in May 2019 but it regained all the lost ground in the following month. Quite the shrug.

And yet we are expected to think that recent market volatility comes from a wildly unpredictable President. Mentions of the word “uncertainty” in the Federal Reserve’s Beige Book have skyrocketed (chart from George Pearkes):

This chart usefully goes back to 1970. Amongst other historical shocks, it covers the oil price spike of the 70s, Star Wars defense fears of the 80s, the dot com bust, the global financial crisis and the first pandemic in a century. But apparently right now is really uncertain. There could be a plethora of reasons, including: the internet has forced people to engage with the true extent of global horrors; information overload; a snowflake society; or the respondents fear they’ll look stupid if they get things wrong so they just say it looks very uncertain. It could be all or none of these. But one conclusion we can safely draw is that it reflects people are currently feeling an underlying vulnerability. Psychologists of the future might trace this back to the technological revolution distancing us from our own instincts, exacerbated by the traumatic experience of living through a pandemic, broadcast globally into the palms of our hands in real time.

But the uncertainty is not Trump’s tariffs. They’re certain. He’s had the same views for decades and already used the same playbook in his first term. (Click here to listen to our CEO Helen Thomas discuss this with BBC News).

So what’s changed this time round to cause the world to be gripped by such uncertainty? The economic backdrop of higher inflation, interest rates and government debt, combined with Trump’s great power both domestically and globally.

The imbalance of the latter is causing a great deal of uncertainty as dysfunctional governments chosen by fractured electorates scramble to respond to Trump’s agenda. Canada’s new Prime Minister isn’t a member of parliament. Neither is France’s. Portugal’s Prime Minister just lost a vote of no confidence over a corruption scandal but will remain in post until elections in May. Germany hasn’t selected its new Chancellor yet but Friedrich Merz hasn’t let that stop him taking a wrecking ball to constitutional spending prudence, in direct opposition to the platform on which he ran in an election held only nine days earlier. And to get his way, he reconvened the old parliament that the electorate had just voted out. This allowed Christian Lindner, who is no longer an MP and whose entire party failed to gain representation in the election of 23 February, to ask the absolutely fair question in parliament just last week, “You, there, sitting in the front row. Who are you and what have you done with Friedrich Merz?”.

2. Germany

Whatever the constitutional niceties, and we can expect to hear more about them when the new parliament sits from Tuesday 25th March, the markets seem happy that a German economy with no growth has at least given itself a chance of growing by loosening the debt brake and investing in defence and infrastructure. Bundesbank boss Joachim Nagel is already lining up the excuses in case it doesn’t, saying US tariffs mean Germany “could expect a recession for this year too”. Bundesbank forecasts only had the economy growing by +0.2% this year without tariffs anyway.

The Zeitenwendewende does not come without risks. T Rowe Price’s chief European economist Tomasz Wieladek warned in the FT that suddenly increasing the supply of a very scarce asset can create instability that extends beyond its own price. This chart shows how the free float differential between German and US bonds correlates to the real yield differential:

In short, a sell off in German bonds could have contagion to other bond markets. We will be keeping an eye on German bond auctions from now on: there’s a 30y on Wednesday, 5y on Tuesday 25 March and 15y on Wednesday 26 March. France, with its 112% debt-to-GDP ratio and lack of functional government to reduce the deficit by the magnitude required, is unlikely to escape unharmed once any sell off in bonds gathers pace.

3. The UK

Step forward Rachel Reeves, who now has to deliver a spring statement alongside the OBR update on Wednesday 26 March, at exactly the moment when markets are sitting on the knife edge of a new world order. Rather boldly, she will be doing this between two Gilt auctions, a 20yr on Tuesday 25 March and a 7yr on Thursday 27 March, along with the latest UK inflation print released on the very morning of her statement.

She is already up against it. The OBR has announced its market data came from the 10 working days up to 12th February and the UK 10yr yield is already ~20bps higher than the average of that period. Meanwhile Starmer has had his Falklands moment and committed to higher defence spending. The long awaited reforms to welfare spending were supposed to provide an offsetting saving but disquiet amongst Cabinet members, not just Labour backbenchers, will see some scaling back of the plans.

Discussions with market participants are yet to reflect the difficulty of squaring this circle: almost all of them believe she will do as she has said and stick to the fiscal rules no matter what, even if it means spending cuts and tax rises. She wasn’t even supposed to be announcing any changes at this spring statement – her Mais Lecture committed to ‘a single autumn budget every year‘ and the newly legislated Charter for Budget Responsibility means the government can only adopt “fiscally significant” measures if they’re also accompanied by a new OBR forecast. This spring update is just supposed to be the point when ‘the OBR will make an updated judgement on whether policy announced to that date remains consistent with a greater than 50 % chance of achieving or exceeding the fiscal mandate‘. In other words, an update on the Budget, rather than anything new.

Except the legislation now means that if the government does want to do something fiscally significant before the next autumn budget, it will need a whole new OBR forecast. If it tried to do that without one, the OBR are at liberty to trigger the ‘fiscal lock’ and provide one anyway. This was all designed to avoid becoming Liz Truss but it is needlessly tying the hands of the government when it needs to be fleet of foot. A man who isn’t even the Chancellor of Germany just ripped up seven decades of fiscal prudence less than two weeks after an election where he promised the opposite… can’t the UK government just do something similar, argue discomfited Labour MPs?

No, not without a radical new plan to convince markets, which would involve jettisoning everything done so far. Taxes on jobs and farmers, fewer benefits for pensioners and the disabled, pay rises for train drivers, more rights for employees AND an extra 0.2 pct pt of GDP for defence don’t add up to a convincing plan to deal with 100% debt to GDP. Labour have a majority but have struggled to convince even their own voters about their mandate. Tweaking to meet OBR forecasts makes the problem worse. Reeves’ plans will likely be out of date before she even sits down at the despatch box after her statement. UK gilt prices will then be out of her hands.

The Bank of England could try to smooth matters with an interest rate cut on Thursday. They have a nice excuse with the negative GDP release for January but they have a problem – inflation remains sticky and, worse, inflation expectations just picked back up, as Reuters’ Andy Bruce pointed out:

We think Catherine Mann will still vote for an interest rate cut, despite the majority of the MPC sticking with their line that ‘gradual and careful approach to the further withdrawal of monetary policy restraint was appropriate‘. Mann argued in her latest speech that ‘I need to look six to nine months ahead for sources of inflationary pressures. Incoming data evidences more extensive weakness in market sector output and consumer demand’. Famously we can no longer rely on the UK jobs report (ignore it again on Thursday) due to the ONS updating its methodology but Mann can see the slowdown hoving into view. She argues that central banks must ditch caution because ‘Gradualism as the preferred monetary policy strategy was promulgated at a time when financial flows were small and the markets more stable… these days, the volatility is coming from financial markets, including (especially) cross-border spillovers’. As she points out, central bank steadiness has hardly translated into stable market pricing, with UK front end rates moving in a range of 100bp even when the BOE was on hold in the first half of 2024:

If Mann can convince the rest of the committee to signal dovishness ahead, GBP might bear the brunt and the currency can do some of the monetary easing for them.

4. The Fed

So, which is it? Trump tariffs reigniting inflation? Trump crashing aggregate demand by cutting government spending? The latest Michigan survey showed politically independent respondents expecting both higher inflation and higher unemployment ahead:

As Renaissance Macro put it, ‘nobody is asking for a raise in this environment’:

Which, if true, would reduce the risk of a wage price spiral and the labour market softens. But if Trump is restricting immigration won’t that decrease the labour supply too, potentially propping up wages? And if he’s getting Congress to extend tax cuts, won’t that stimulate aggregate demand? What about the promised deregulation that is designed to encourage the private sector to take over from a cut back public sector?

Until the answers are clearer, Powell won’t want to say a word. He will try to sit back when the Fed meet on Wednesday. He needs to let more of this play out. The attention is all on Trump and he will be happy to leave it that way. The dot plot will provide potential for additional volatility as political ideologies drive FOMC members to move their dots, depending on whether they support Trump’s plan or not. Whatever their views, the Fed is not about to bowl into proceedings and provide a backstop to a volatile stock market.

5. The BOJ

With the BOJ having been burned by market volatility in the wake of their hike last summer, they will not rush to raise rates again on Wednesday. Governor Ueda is still likely to sound hawkish given the springtime shunto wage rounds. He told parliament “wages… continue to rise steadily. As such, we expect real wages and consumption to improve ahead“. The Japanese Trade Union Confederation just confirmed the biggest pay hike for its members in 34 years.

6. Gamma

No rescue from the Fed. Tighter policy from Japan. Huge geopolitical risk. The MAG7 stocks chastened as earnings expectations turn negative:

Travel stocks plummeting: United Airlines revenue from government travel was $1bn per year, now reduced with fewer government workers thanks to DOGE. Confused consumers scaling back travel plans in the US:

And gamma has plunged to its lowest level in over a year, meaning that all of these fundamental factors can finally be priced into a market that had simply been consumed with buying-the-dip, come what may. With the VIX still remarkably quiescent and the FOMO buyers still present, we are due a much bigger market wobble in the two weeks ahead. The beatings will continue until morale improves. This is a sensible moment to reassess the assumptions that have underpinned your investments for the last few years. It Will All Come To Aught.