The Two Weeks That Will Be (14th June 2026)

1. The UK

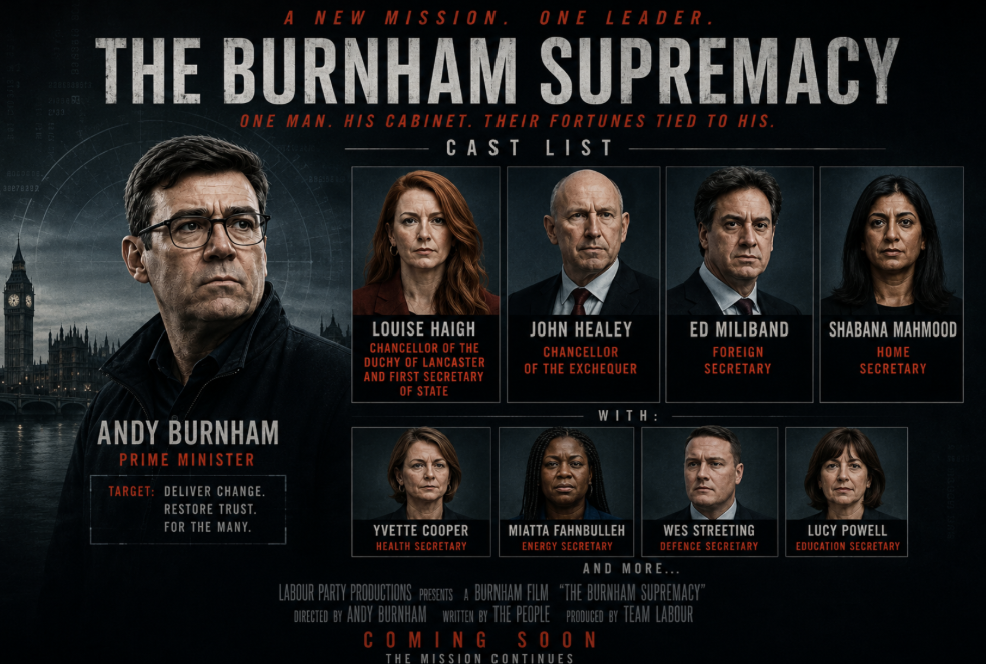

The Burnham Identity is about to give way to the Burnham Supremacy. In the early hours of Friday morning, power passes from Keir Starmer to Andy Burnham following the Makerfield by-election. The man who has lost four cabinet ministers and his chief of staff, had 100 of his own MPs and eleven trade unions call for a timetable for his departure, and presided over disastrous local elections along with the loss of a Labour government in Wales cannot continue. He will be replaced by a man who holds the most potent ace card: that he was not a part of the administration that has so precipitously lost its way. His is a clean pair of hands, no trace of the blood into which every other wannabe challenger had theirs dipped. His hand also holds the hint of a royal flush because he is a proven winner: already three times victor in the Greater Manchester mayoralty on two-thirds of the vote, he can then add to the trophy cabinet that he is vanquisher of the nation’s most consequential politician and scourge of the left, Nigel Farage.

And on that morning he will hold maximum power. The possibility of patronage will keep Labour’s fratricidal tendencies at bay, with factions unwilling to take down their internal opponents for fear it weakens their own position. To govern is to choose but in those liminal moments, between leisure centre podium and Downing Street, Andy won’t have to choose much at all. So far he’s told us that he will stick to the fiscal rules, keep the triple lock, consider something for WASPI women, get people out of welfare and into work and scrap business rates for hairdressers.

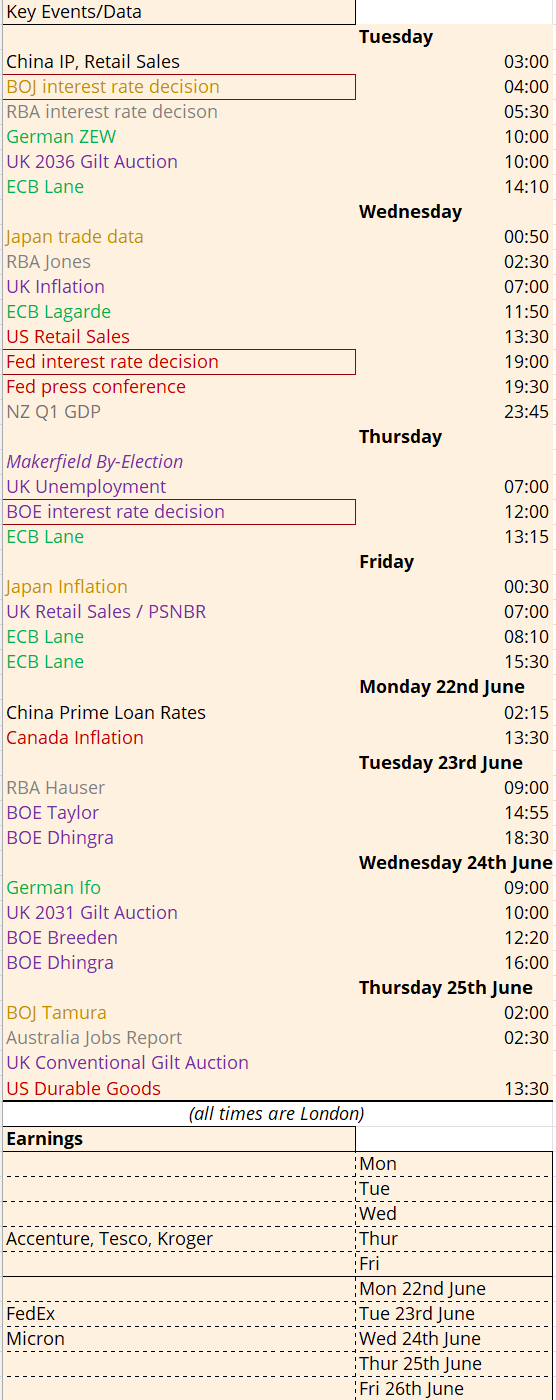

How? This question will be so persistent as to minimise both Burnham’s honeymoon and Starmer’s notice period. Given the Greater Manchester Mayoral election is slated to take place on Thursday 30th July, and Parliament goes into recess on Thursday 16th July, Burnham’s team seem to think they have time to get their act together. This misconception will very quickly become clear. Burnham will hardly be able to draw breath from his victory speech before the media questions will begin. Hey Andy, there’s a NATO summit on 7th July, how would you get a Defence Investment Plan that’s fit for purpose? What would be in your Budget, which in two months the OBR will have to start preparing, will you be raising taxes or cutting welfare? And let’s have a quick look at government borrowing, released just hours after the by-election result on Friday at 7am, how will you keep on top of that? Andy? Andy…?

And every time Andy is asked, it becomes more clear that Keir is not. The UK constitution doesn’t allow for there to be no prime minister but nor does it allow for there to be two. The Labour Party might only have been in government for a quarter of its existence, rarely facing the need to confront leadership challenges, but government rather than opposition makes necessity the mother of invention. Financial markets price in probable outcomes; the longer and more tortuous a change of leadership, the more volatility in the price of British assets. And the more costly that becomes for the British state, the harder it will make the task of the next Labour leader.

Burnham should use the momentum of his election victory to mount a leadership challenge with such a numerical advantage of MP backers that it not only renders an alternative challenger redundant, but mathematically humiliates Starmer into submission. If not, then financial markets will price in the uncertainty to such a degree that fiscal space is eroded and/or currency depreciation adds unhelpful fuel to the inflationary fire.

There may be somnolent markets during the prime ministerial interregnum; in the summer of 2022, post-Boris and pre-Truss, the BOE managed to raise rates twice (including the August 50bp hike). But this time round, base rates are already twice as high and Gilt issuance is due to be 50% higher this fiscal year than it was in 2022-23. In the face of this particular regime change, the Bank of England will leave rates unchanged on Thursday. There are likely to be at least two dissenters, with speeches already slated in the subsequent week from Taylor and Dhingra on Tuesday 23rd June and Breeden on Wednesday 24th June. The latter date also sees a 5y Gilt auction with another conventional Gilt auction on Thursday 25th June.

2. The US

Trump has turned 80, there’s cage fighting on the White House lawn and the biggest World Cup ever has begun in the Americas. There’s just the small matter of a memorandum of understanding to sign with the Iranians, which will mostly kick the can down the road whilst declaring in word, if not deed, that the Strait of Hormuz has miraculously re-opened. SpaceX is up and floating (or rather floating and up), adding yet another trillion dollar market cap company to the US roster.

New Fed Chair Kevin Warsh will not want to spoil the party atmosphere. On Wednesday there will be no change to interest rates but we will be left in no doubt that the institution is under new management. It’s the beginning of the end of the dot plot. Press conferences will be fewer and shorter. Flexibility will be the name of the game. With plausible deniability Warsh can protect himself from political attacks whilst preserving the power of the pulpit. As he put it in the FOMC meeting on 30-31 January 2007, “we should use a ‘benevolent leader’ model“. This is not the unilateral decision making of a benevolent dictator but nor is it simply representing a consensus of the committee average. “I don’t view the Chairman, in his testimony or in his announcement of projections, as the press spokesman for the FOMC“.

He clarified of the position of Fed Chair: “Those are his views. But second, and very much alongside his views, he would present our views. His presentation of our views is useful in making certain that a lot of attention is focused on them… in some ways we might well be delegating to him the ability to draw a central tendency and make appropriate conclusions“.

This is something of a return to the Greenspan era, when the Humphrey Hawkins testimony was almost all that mattered for understanding the direction of the Fed. Press conferences and dot plots were far more relevant when monetary policy was constrained by the zero lower bound and central banks were desperate to slay the deflationary demon of doom. But in a world of more normal levels of interest rates and inflation, central banks don’t need to massage basis points onto low and flat yield curves in order to squeeze another drop from the stimulatory lemon of monetary policy.

3. The BOJ

If ever there were a sign that the post financial crisis deflation era is over, it’s that even the Bank of Japan will raise interest rates on Tuesday. Unfortunately Governor Ueda will not be participating, having been hospitalised for treatment for an infected liver cyst. This is the first time a governor has missed a scheduled meeting since the current monetary policy arrangement was established in 1998.

It means that Deputy Governor Uchida will take the post-meeting press conference and whilst considered a safe pair of hands, it raises the risk of volatility, particularly with the Yen balanced precariously at its pre-intervention lows. The BOJ had already been taking baby steps in tightening policy, careful of the looser fiscal policy emanating from new PM Takaichi. With Ueda pivotal to expectations management, his absence from the meeting suggests no firm conclusions will be drawn until his anticipated return at the next meeting at the end of July.

It also opens up another potential scenario. If Ueda were to become permanently unavailable then Takaichi would be afforded the opportunity experienced by her political patron Shinzo Abe – appointing a new central bank governor to run monetary policy in coordination with fiscal policy. Takaichi might then be able to reach for three arrows of her own.