The Two Weeks That Will Be (16th February 2025)

1. Germany

Germans go to the polls on Sunday and predicting the outcome is complicated by two elements of the electoral system:

- The 5% threshold to gain electoral representation.

- Currently three parties are polling below this level, including a party formerly in the governing coalition, the FDP.

- There is also an exception to the 5% hurdle – if a party wins three constituency seats, they still make it through.

- All of this means anywhere between four and nine parties could hold seats in parliament.

- The new fixed 630 seats for the Bundestag.

- Electoral law reform passed in 2023 has now set the number of seats at 630.

- Previously, the number of representatives had to be adjusted upwards to ensure proportionality to balance out the voting system which has two votes: a first-past-the-post vote for a constituency MP and then a second vote for a party.

- Here is a schematic from the American-German Institute showing just how “clear” this is:

These electoral quirks might have had only a small impact in a stable system. But the German electorate has become just as fragmented as any other in the western world. Support has been ebbing away from traditional parties and seeking out the new. Even at the last election the two main parties in Germany fell below half of the popular vote:

More than a quarter of German voters claimed they are undecided with just over a week to go. The AfD are in second place in opinion polls, despite only coming into existence in 2013; four years ago they were at 10.4% and now they’re polling at double that. With voters afraid to reveal their preferences, their true support might be even higher and could be boosted by potential split ticket voting under the new electoral system. In the prior regime, overhang seats were awarded to create proportionality, leading to 736 members last time round, the largest freely elected parliament in the world and considered rather unwieldy. This time, seats will be denied to parties in order to fix the total number of MPs. What better way to protest against the old parties than giving your second vote to a protest party and denying the old guard representation?

Despite the uncertainty, the market appears relaxed, working on the blasé

assumption that the old guard will band together come what may. Except that the grand coalitions and three-party coalitions of the last few parliaments have led to increased voter discontent and stagnation for the German economy. Why would the CDU/CSU want to work with the SPD and the Greens when the latter two parties have been discredited by their past failure in government? Let alone that their remedies for solving Germany’s problems are diametrically opposed: tax cuts from the right, spending rises from the left.

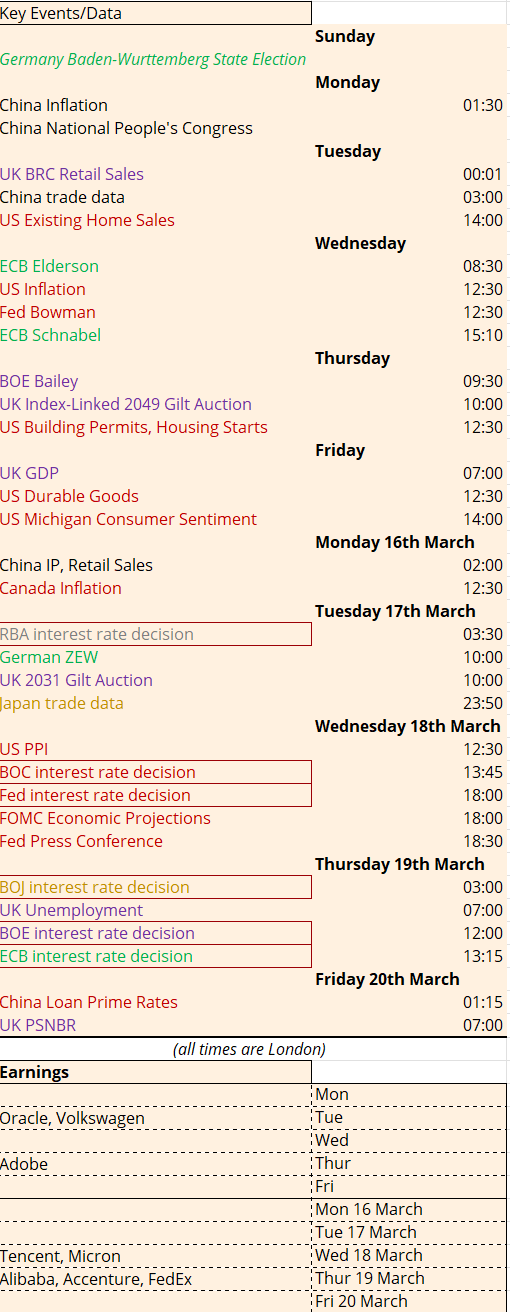

The raft of German data released in the week after the election will only serve to highlight the scale of the challenge facing whoever makes up the next government: IFO on Monday 24 February, Consumer Confidence on Wednesday 26 February and Inflation on Friday 28 February.

There is another blasé assumption, that simply loosening the debt brake would address all the country’s problems. Even the Bundesbank has been urging reform, whilst the probable next Chancellor, the CDU’s Friedrich Merz, admitted in an election debate that “I did say that we can discuss everything”. But as this FT article from Tomasz Wieladek, chief European Economist at T Rowe Price, pointed out, extra bond issuance isn’t exactly what a world bursting at the seams with government debt needs. He argues that the scarcity of Bunds had kept their yields artificially low, such that increasing their supply would take yields higher – potentially dragging US yields up along with it:

It might be hard to imagine that a country with a debt-to-GDP ratio of 64% would struggle to sell its debt in a world where its neighbour in France has a ratio of almost double that. It should be easier to imagine that both countries are part of a currency union where the cumulative persistent failure of its two core countries to meet the Maastricht criteria infects the debt sustainability of the entire project. For now, the market has decided that pooling credit risk between Eurozone nations plus an alleged ECB backstop means that the risk premium for Germany and France is lower than it would be if they were outside the monetary union. One day this will come to look more like how AAA rated CDOs were dragged down by the polluting toxic debt of their constituent parts.

2. The UK

Unfortunately for Rachel Reeves, this benevolent pass for the political risk inherent in the Eurozone has landed all the debt-sustainability attention at her door. Leaks from the first round of the OBR forecast process suggest that her fiscal headroom has already disappeared. The most senior civil servant in the Treasury might have ordered an inquiry into the leak but that’s not so much shutting the stable door as finding the stable has burnt down and the horses are in the glue factory.

Reeves has run out of road.

The PM and the Foreign Secretary have both publicly overruled her attempts to keep a lid on defence spending given developments over Ukraine. The BBC ran a thorough investigation into two stories that had been floating around for some time, that the Chancellor was embroiled in an expenses investigation whilst working at HBOS and that she exaggerated her CV. The BBC spoke to “more than 20 people, many of whom were former colleagues, and gaining access to receipts, emails and other documents“. They include screenshots of receipts from Christmas 2008, where, in the aftermath of Lehman going under and as HBOS itself was struggling to survive, Reeves bought a £49 handbag for her PA.

That might have been a simple motivational gift but a whistleblower felt it went against company policy, and they were perturbed enough by the issue to keep hold of the evidence for over 16 years. In the world of politics this kind of matter can blow over, but only if you have the support of your party.

And so we can start to assume that Pat McFadden will be delivering the statement alongside the updated OBR forecasts on 26th March. A safe pair of hands, steeped in the party, and full of experience which includes the Blair/Brown years, he could steer the ship into steadier waters.

But he’s not a miracle worker. We will get the latest inflation data on Wednesday and more importantly the Public Sector Net Borrowing number on Friday. This latter number is the big one, not just because at the last reading it showed the government was already borrowing £4bn more than the OBR had forecast, but because it’s the big month for the government to get money into its coffers. January is tax return deadline month and is the one month where the government reports a surplus, as you can see from the positive bars in this chart (absent the pandemic period):

The government needs this January to be a big one otherwise borrowing numbers are going to increase, no matter what the OBR delivers in March. There are two Gilt auctions to watch: a 40yr on Tuesday and a 4yr on Wednesday. However it’s tough to assess genuine demand with recent auctions having been conducted by syndication – the most recent on 11 February was the highest amount sold via syndication since May 2020 during the white heat of the pandemic. The DMO said they increased the size of the auction due to demand.

At least the OBR has already locked in Gilt yields for its forecast. If we assume that they’re using a similar timetable to the October process, the market data, including the levels of GBP and bond yields, will have been taken as an average during the period 23 January – 6 February. That would put 10y yields around 4.55% rather than nearer the 4.90% we saw at the start of the year. The only trouble for the OBR is that they also offer a sensitivity analysis in their forecast whereby they explain what move in yields (and other data such as inflation) would see the fiscal rules breached. This leaves them open to the possibility that the market might have already made such a move by the time their model is published. Which rather poses the question of why the Chancellor and the market is waiting for the OBR, rather than judging the sustainability of government debt by the merits of the government’s plan.

3. Trump

The new President is pursuing his plan with extreme prejudice. Never one to let conventional niceties get in the way, DJT is already planning to get MBS to host talks with Russia in Saudi Arabia in the days ahead. European leaders have merely been sent a questionnaire from the US about what security contributions it could provide for Ukraine.

The shock here should not be an energetic and enthusiastic Trump getting stuck in. He has all the power right now and time will leech it from him. He knows he needs to press his advantage whilst he has it. He said he would cut government spending, deport illegal immigrants, impose tariffs and settle conflict in Ukraine – now that, in his mind, he’s on his way to all of those, he will focus on his other promises, in particular extending tax cuts. The pace is not going to let up. The real focus should be on the other players in each of these games: which countries are going to work with the US and which believe they’re better off getting their retaliation in first?

4. Earnings

Whilst political risk is running high, we might all take a moment to hear from the wisdom of a man in his nineties who has seen much of it all before. Berkshire Hathaway is due to report earnings on Monday 24 February. In their last press release, if it can be called that, Warren Buffett mused that “As I write this, I continue my lucky streak that began in 1930 with my birth in the United States as a white male…. So favored by my male status, very early on I had confidence that I would become rich. But in no way did I, or anyone else, dream of the fortunes that have become attainable in America during the last few decades. It has been mind-blowing… Things didn’t look great when I arrived at the beginning of The Great Depression. But the real action from compounding takes place in the final twenty years of a lifetime. By not stepping on any banana peels, I now remain in circulation at 94 with huge sums in savings – call these units of deferred consumption – that can be passed along to others who were given a very short straw at birth“.

Investors will be hoping Nvidia doesn’t disrupt the compounding in their portfolios when it reports on Wednesday 26 February.