The Two Weeks That Will Be (6th July 2025)

The tears of a UK Chancellor would not normally trouble Gilt investors, unless they reflected, whether intentionally or not, the physical manifestation of an unstoppable political force meeting an immovable fiscal object. The detail of the government’s welfare reforms were scrambled together to ensure meeting the fiscal rules for the Spring Statement, only to unravel at the last minute as they failed to meet the political priorities of too great a minority of Labour MPs. The Chancellor would be entitled to an expression of frustration as she has spent her entire time in office trying to avoid a Truss moment, only to see a rebellion by her own party deliver the largest move in UK 10 year yields since the October 2022 Truss debacle.

Except it is the Chancellor’s interpretation of this episode that caused the problem in the first place. Every decision has been driven by the need to ensure the OBR declares the fiscal rules have been met rather than more broadly delivering a credible plan. Sunak fell victim to the same obsessional spreadsheet optimisation but politicians must also be salespeople. The country understands there are fiscal constraints but wants to know what you will prioritise to work through them. Who does the government care about? With pain inflicted on pensioners, farmers, businesses and the disabled, it has not always been easy to know.

Reeves’ first act was to agree to public sector pay rises partly in order to remove industrial action from weighing down OBR growth forecasts (dedicating a whole annex to this in the Policy Paper) but then cut the winter fuel allowance to try to pay for part of this.

The £9.4bn for pay rises formed almost half of the now infamous £22bn black hole:

To offset this, efficiency savings would do most of the work, followed by the cut in winter fuel allowance:

The bonus, if you’re focused on the OBR, is that winter fuel allowance eligibility is calculated from mid-September, thus giving enough time for this reduction to be factored into the OBR model ahead of the Budget. The negative is that this decision became known as the government’s original sin. They failed to sell the policy, leaving it floating in the summertime vacuum, with 12 weeks given to the OBR for their modelling process before Reeves would deliver her first Budget. One year on, this word cloud by the pollsters More In Common shows how it has become such a catastrophic totem:

We warned after this decision that “the real opposition is the Labour Party itself… There will be those within the party who will chafe against the restrictions of the inflexible Chancellor and the unelected OBR”. It might have been written off as an early mis-step but the obsession with pleasing the OBR continued to lay political landmines. The Budget hiked taxes on jobs, farmers and family businesses. The Spring Statement sought to withdraw benefits from the disabled. Again and again, policy measures were seen to be taken only to satisfy the fiscal rules rather than as part of a political plan.

The adjustment to Personal Independence Payments (PIP) was the ultimate in spreadsheet-ification, reducing the assessment of whether a person could, for example, wash below their waist into a table of cost savings:

You can see from this table that the OBR weren’t even sure about those savings, putting them at “Very High” levels of uncertainty. It doesn’t matter now, because the extent of the Labour rebellion means they have been removed from the legislation until the so-called Timms review is complete. And so the measures announced in March to meet the fiscal rule on the current balance have not been enacted, meaning the rule is no longer being met:

No wonder Rachel was in tears. Her homework will be returned covered in red ink. Ever-higher Gilt yields reflect the self-confessed girly swot must do better.

But she can’t. Our analysis of the Welfare Rebellion demonstrated the breadth of Labour dissatisfaction spread well beyond the left tail of wanton troublemakers into more centrist moderate MPs:

The market has so far concluded that adding this political constraint to the fiscal constraint means the gap must be filled by tax rises. Reeves alluded to as much in her interview with the Guardian, admitting “I’m not going to apologise for making sure the numbers add up. But we do need to make sure that we’re telling a story, and a Labour story”.

She got the memo that policy cannot only be decided by the OBR – now it must have a narrative attached. Although that might please Labour MPs and Labour voters, it will perturb the markets. As one Gilt investor put it to us last year, “Why should I finance pay rises for ASLEF?”. Reeves will not have assuaged their concern when she went on “I made it really clear that priorities in that budget were to protect working people, to invest in the NHS and to start rebuilding Britain“. None of these things scream generating growth to ensure debt sustainability: The NHS is a low growth multiplier, planning reforms take decades to bear fruit and protecting working people appears to mean taxes on business owners or anyone with any assets. Given the manifesto commitment not to raise the three big taxes, it’s clear that taxes will increase on everything else, whether its pensions or second homes or banks or ISAs.

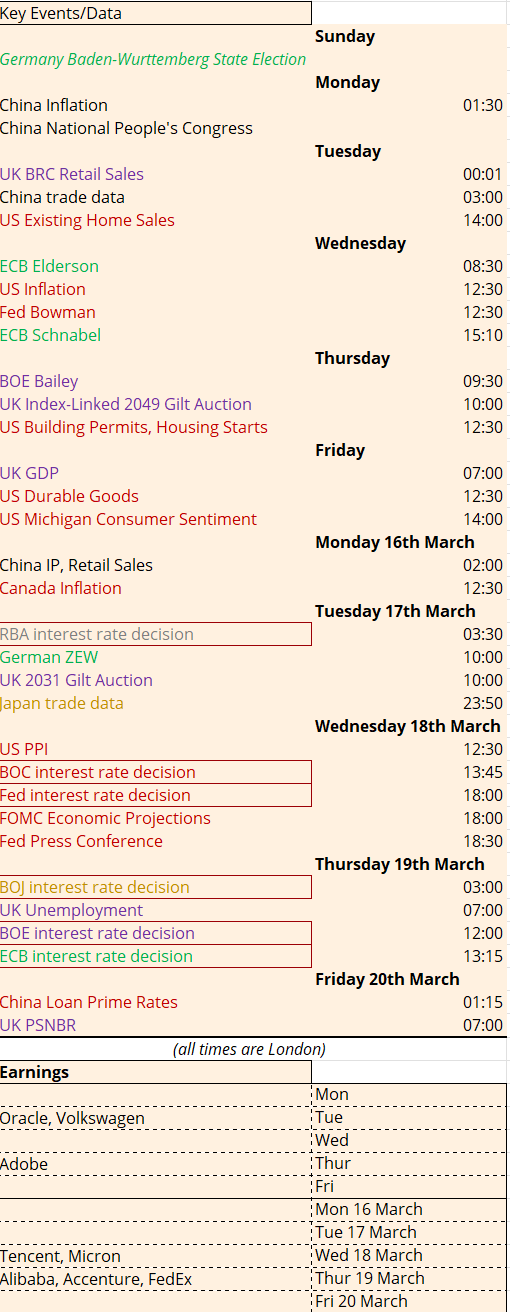

Speculation about this, as much as its implementation, will weigh on already anaemic growth. We will get the latest GDP data on Friday along with inflation on Wednesday 16th July. The latter might harm the Bank of England’s dovish inclinations although Governor Bailey can reassert them at his Mansion House speech on Tuesday 15th July.

And tax hikes don’t in and of themselves necessarily deliver increased revenues. We are about to see the Laffer Curve tested out in real time. The OBR noted in its March update that they got their revenue forecast wrong: ‘The shortfall in 202425 against the October forecast is mainly due to lower-than-expected outturn receipts from corporation tax, self-assessed income tax, and capital gains tax. Much of this shortfall relates to 2023-24 liabilities and suggests that small company profits, partnership income, and dividends were more depressed than we expected by that year’s high and externally driven inflation and high interest rates‘. Since then they have released their annual Forecast Evaluation Report and noted that they had serially overestimated growth and productivity. The OBR will have more updates on this in its latest Fiscal Risks and Sustainability Report on Tuesday. Downgrades to its forecasts would make the gap to fill even more insurmountable. The Bank of England’s FPC should mention these risks in its latest Financial Stability Report on Wednesday.

An uncertain OBR plus a wobbly Chancellor leads to comments such as these from the CIO of Legal & General Investment Management: “[Markets] can’t trust that what’s been put forward will be put in place”. The CIO of core investments at AXA Investment Management summed it up: “Keeping the markets on side is at odds with maintaining support amongst Labour’s traditional base. The gilt market will remain very sensitive to any signs of political or fiscal weakness in the months ahead.” Gilt investors might think all manner of tax rises can satisfy the OBR but two thirds of voters think the government’s fiscal rules will be broken, according to a More in Common poll.

We maintain that the political and fiscal constraints are irreconcilable and the gilt market will have to give. Once it does, higher gilt yields in the long end will turn the spreadsheet to dust, rendering the Chancellor and the OBR redundant.

It’s not just events in the UK that can cause bond market wobbles. The deadline for the pause on Trump’s tariffs kicks in on Wednesday although there are already signs that this might slip for countries who are negotiating ‘in good faith’. Japan and the EU will be the toughest nuts to crack, with the former worried about the Upper House election on Sunday 20th July and the latter inevitably struggling to find consensus. Von der Leyen has admitted the ambition has been reduced to an “agreement in principle” between the EU and US. Noise will increase as both sides attempt brinkmanship but Trump is in the ascendance having passed the Big Beautiful Bill by the Independence Day holiday as he had promised.

Earnings season kicks in from Tuesday 15th July, starting with JP Morgan and BlackRock, throwing in the potential for extra volatility. Liquidity will also start to thin as we head into the summer. Risks are building as electorates remain restive and Trump flexes his muscles. As long as the VIX index remains below 25 then the FOMO impulse will keep stock markets rising; above there we enter the sudden pricing in of all the risk that has been bubbling under the surface.

To conclude on an upbeat note, have a listen to our latest podcast with Alex Patelis, former Chief Economic Adviser to the Greek Prime Minister. It is ten years ago that the Greeks decisively voted No in the referendum on a bailout – only for the recently elected Prime Minister Alexis Tsipras to cave in and accept even harsher austerity bailout terms three weeks later. Now, Greece is running a primary budget surplus, its government bond yields are below that of Italy, and its debt has returned to investment grade. How did it do it? Listen or Watch to find out…