The Two Weeks That Will Be (8th March 2026)

Greenland, Venezuela, Iran, Cuba? One by one, the US is removing China’s pieces off the board. Or at least attempting to do so. It is no easy task, given disruption of China’s supply chains of commodities and influence runs through the worlds of narcoterrorism and unpleasant regimes. But it is one that a man who grew up in Manhattan real estate might be more psychologically disposed to interact with than most. Forget bringing guns to a knife fight, if President Trump can deploy an aircraft carrier to the negotiating table then he will do so. Bullying? Naive? Insane genius ready to plunge one of the most inflammatory regions in the world into flames in order to get a deal with his main adversary? Whatever the answer, the outcome will be the same: a protracted period of instability in the Middle East that raises the price of key commodities.

The price of oil is going up but it will be volatile. Trump will want to declare victory after victory, even if ships can only transit the Strait of Hormuz with a US escort and insurance underwritten by the US government. China has just announced its lowest GDP target for the year since 1991 and is in the midst of its National People’s Congress. Trump is slated to meet with Chinese President Xi from 31 March to 2 April and will want to ensure he’s in pole position by then. That doesn’t necessarily mean a democratically elected leader for Iran, or that Iran has had its military capabilities permanently eradicated – just that he’s done the job of warning China that they face a strong adversary. Trump’s 1987 full page advert said it all – just substitute the word “China” for “Japan”:

“The saga continues unabated as we defend the Persian Gulf, an area of only marginal significance to the United States for its oil supplies, but one upon which Japan and others are almost totally dependent. Why are these nations not paying the United States for the human lives and billions of dollars we are losing to protect their interests?

Saudi Arabia, a country whose very existence is in the hands of the United States, last week refused to allow us to use their mine sweepers (which are, sadly, far more advanced than ours) to police the Gulf. The world is laughing at America’s politicians as we protect ships we don’t own, carrying oil we don’t need, destined for allies who won’t help“.

He concludes “It’s time for us to end our vast deficits by making Japan, and others who can afford it, pay. Our world protection is worth hundreds of billions of dollars to these countries, and their stake in their protection is far greater than ours… Tax these wealthy nations, not America. End our huge deficits, reduce our taxes, and let America’s economy grow unencumbered by the cost of defending those who can easily afford to pay us for the defense of their freedom”.

Forty years have not changed the man. For Trump, the economic and national security umbrella of the United States must be rebalanced to benefit the US. If he is satisfied of that following his meeting with President Xi, he will roll onto the next items on his agenda: his 80th birthday celebration, the FIFA World Cup and celebrating 250 years of US independence.

But removing heads of state on his path to constraining China doesn’t come cheap. There is a reason politics can’t easily be conducted by businesspeople: voters. Trump does better than most in terms of winning over the voters he needs but when it comes to foreign policy he’s not operating in a vaccuum. He might win the ratings war in America but the other players in the game have different motives. Some allies might be better served by deliberately opposing Trump’s policies – as Denmark’s PM Mette Fredriksen recently found over Greenland:

The equivalent tracker for Trump is so skewed by the two party system in America as for it to be almost redundant. His approval rating is falling amongst registered independents but this is still vastly outweighed by the fact that Democrats disapprove of him almost as strongly as Republicans approve:

Independents:

Democrats:

Republicans:

And the Middle East itself is a whole other chessboard. President Trump might have a plan for what victory in his game looks like, but the ongoing instability of a post-Ayatollah Iran having fired on its regional neighbours is unlikely to see the region find a stable equilibrium any time soon. A US aircraft carrier might remain as a policeman for the Strait of Hormuz but the risk of a wayward drone or accidental insurgency could bog many countries down in the region for some time to come.

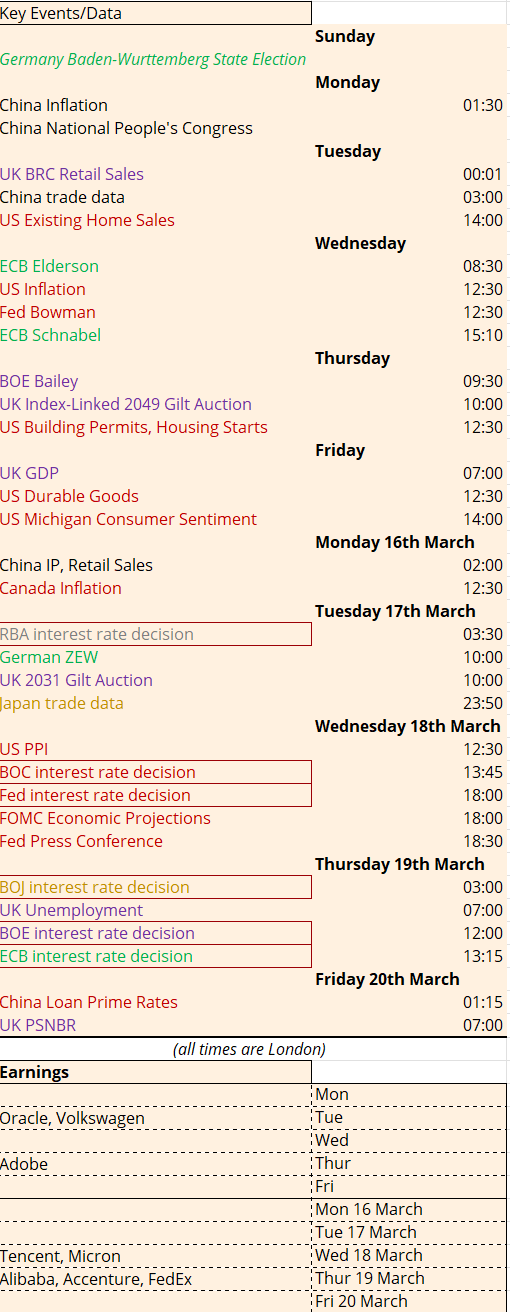

This will leave many of the world’s central banks facing yet another inflationary surge. Do they consider it demand destructive or simply a one-off supply shock? There will be strong political pressure on the Fed to look through the inflationary impact. Waller has already batted away concerns, saying “It’s kind of very odd to think about the Fed maybe changing rates six months from now based on this”. It does rather render redundant the inflation print on Wednesday, although all US data is now in the dock following the surprise negative payrolls print for February. The FOMC can use the fog to ignore the cockpit instruments and light their own way forward with the latest Summary of Economic Projections at their meeting on Wednesday 18th March. The press conference will likely be the penultimate one for Jerome Powell with Kevin Warsh’s nomination now formally sent to the Senate.

The central bank decisions come thick and fast with the Bank of Japan, Bank of England and ECB all holding meetings on Thursday 19th March. None of them will want to do anything during such a period of uncertainty. The ECB will be pleased that markets are starting to price in hikes as that will do some of their work for them; the Bank of Japan will signal a cautious hawkish hold after sources rowed back on Ueda’s suggestion of imminent rate hikes; and at the Bank of England Andrew Bailey will not want to change his swing vote into taking action.

With central banks choosing to be in the passenger seat, bonds will continue on the path of least resistance given the return of inflationary risk. The Gilt market has once again demonstrated its vulnerability in such an environment. Almost the entire improvement in the 10y Gilt yield assumption used by the OBR in its updated Spring Forecast has been eradicated by last week’s moves:

Reeves used her statement to argue that the vulnerability means she must be allowed to stick to her course: “because of the action I have taken we are expected to spend nearly £4 billion a year less on debt interest next year than was forecast in the Autumn and if we stay the course and stick to our plan, and our debt interest rates return to the G7 average… we will have £15 billion a year more for the priorities of working people and to make working people better off“.

The £15bn figure seems to come from OBR sensitivity analysis that suggests a 1 pct pt increase in Gilt yields would increase borrowing by that amount (and reduce it by the same if yields fell by the same amount). Given the 10y yield moved by about 40% of that in one week, it seems an unreliable foundation upon which Reeves builds her pitch. And the action she has had to take as the Chancellor of a weak and unpopular govnement has only served to increase vulnerability. Her £4bn less in debt interest has already been used to spend on policy measures as the green bars on this chart of net borrowing from the OBR show:

We will get an update on the PSNBR on Friday 20th March. If Reeves can’t even afford to bank a small improvement, the political vulnerability will act as accelerant for the fiscal vulnerability.

At some point in the next two weeks, Reeves will deliver her second Mais Lecture. She will be the first person to deliver two, perhaps worried you didn’t get the message she set out at her first one in March 2024. In it she quoted a number of radical left-wing economists, claimed Nigel Lawson was “wrong not only in application but in theory“, warned “the analysis on which [New Labour] built was too narrow” and concluded with a flourish that capitalism itself breaks democracy: “a model based on the pursuit of narrow-based, narrowly-shared growth – with ever-diminishing returns – cannot produce adequate returns in growth and living standards, and nor can it command democratic consent.” After almost two years in government she will attempt to explain what her ideology is getting right.

Whilst she goes back to her PPE textbooks, the realpolitik of international relations will pile pressure for increased defence spending onto every country. French President Macron might be embattled but he does at least understand the point of a photo opportunity, delivering his speech on his new doctrine of “forward deterrence” for Europe in front of a suitably threatening nuclear submarine:

German Chancellor Merz proffered the pragmatically candid assessment on US/Israel strikes on Iran that “The criteria of international law will have relatively little effect. … Appeals from Europe, including from Germany, the condemnation of Iranian violations of law, and even extensive sanctions have had little effect … That also has to do with the fact that we were not ready to pursue our fundamental interests with military force if necessary”.

There is the first of five key German state elections of the year taking place today, Sunday, as Baden-Wurttemberg goes to the polls. If Merz’s CDU can regain leadership from the Greens, the Chancellor might feel some vindication for his post-general election Zeitenwende on defence spending. The exit polls suggest he has been thwarted, with the Greens coming out on top.

UK PM Starmer might also hope he’s through the worst, with the Middle East providing a welcome distraction from domestic woes. It may even provide an oppourtunity as much as a challenge. He will feel emboldened that the British public broadly agreed with his position with a YouGov poll showing Britons oppose the US strikes on Iran 49% to 28%. Except that the problem for weak leaders is they are burdened by the reverse Midas Touch. It isn’t just their decisions that they are judged on, but on how they come to them. The public also think Starmer is managing the UK’s response badly with even one third of Labour 2024 voters in agreement:

Starmer may take comfort that a majority of Labour voters think he’s handling it well. But recent polling shows the party could drop from first to fourth in council elections in London in May. Weak leaders who struggle to make decisions at the best of times, who admit they don’t much like politics and are shorn of their closest advisers would struggle to reverse such a weak position. Throw in a defence levy to boost defence spending and an inflationary spike to energy bills for a nation weary of the cost of living, and it’s hard to see where Starmer supposes the win might come from. The PM might be safe for now but he is isolated as the challenges pile up.

Despite the rising political risk, financial markets have largely ignored it over the last twelve months. This is due to the “Don’t Get Caught Short” mentality unleashed by last year’s violent whipsaw in the wake of Liberation Day. When one of the most liquid ETFs in the world, the SPY, printed a 90bp premium to NAV on Wednesday 9th April 2025 as everyone scrambled to cover short positions following the pause on tariffs, it cast a long shadow:

The message from all wobbles since Covid has been to hold on to your long positions – the downside will reverse once the policymakers take action. This has created a perverse situation where implied volatility is pricing in increased risk but not the underlying. As Tier1Alpha pointed out, “The spread between VIX and SPX 1m realized vol, a broad proxy for the volatility risk premium, is now in the 99th percentile”. Either there really isn’t much risk premium out there, or stock markets need to catch up to reality.

And when the catch up comes, it’s big. We have already seen this in oil, where the Crude Oil ETF (USO) had its biggest ever weekly gain. As Charlie Bilello put it, “This was a 6-sigma event, which (assuming a normal distribution) is only supposed to occur once every 4,039,906 years”.

And yet the question at the moment is merely “how long is this war going to last?”, indicative of a market that really doesn’t want to have to take off its long risk positions if they only have to put them all back on again at higher levels. You’d have thought a burning hotel building in Dubai, almost no ships transiting the Strait of Hormuz, the lack of fiscal room for indebted governments and a President on a mission might raise a different question. Like, how high can oil go?

Or, at the very least, do I have a liquid enough portfolio to manage the uncertainty? The Bank of America Fund Manager survey printed record low levels of cash in January – even lower than the pre-financial crisis boom times:

Throw in BlackRock writing down the value of a private loan to zero just three months after assessing it at par, the gates coming down at BlackRock’s private credit fund HPS Corporate Lending and Blackstone injecting extra cash into its private credit fund so that it could meet redemptions and jitters over liquidity could extend.

This is all a function of the platy-leptokurtic market we identified in our year ahead. The upside distribution is platykurtic, with mild upside, but the downside is leptokurtic with a fat negative tail. Pushing this to extremes, imagine that once the VIX breaks above 25, the “Don’t Get Caught Short” narrative flips into “Deleverage Because You’re Too Long” very quickly. We may be about to enter this regime shift, just as the Ides of March approaches.