The Two Weeks That Will Be (31st May 2026)

1. The UK

The Burnham Supremacy approaches. Once Andy wins in Makerfield he will be carried aloft as The Great Farage Conqueror all the way into Number 10. His neighbour at No11 is likely to be Ed Miliband or Yvette Cooper, even as newspapers talk breathlessly of the role being awarded to former Transport secretary Louise Haigh and current Home Secretary Shabana Mahmood. The latter would be best to remain in post, holding the hospital pass of immigration, whilst the latter can deliver significant fiscal reforms to welfare in the Department of Work and Pensions.

Either way, we are just a few weeks from a completely new administration. Whilst the market might remain sanguine that Burnham’s lip service to the fiscal rules remains sacrosanct, change lies ahead.

- Tony Blair has entered the chat, penning an irritable but thoughtfully provocative essay which recommends North Sea drilling, reforming welfare spending, “getting rid of all the old shibboleths” on the NHS, doing ‘whatever it takes’ to stop illegal immigration and ultimately aiming for lower spending and taxes.

- Burnham responded “The lesson from Greater Manchester is that you can’t just leave it to the market, as Tony’s essay seems to suggest. If you want higher growth in areas that don’t have it, you need strong public control and direction over both the investment strategy and the enablers of a more productive economy, such as transport, energy, water, education and housing”.

- Wes Streeting chimed in with “The centre-left’s task is not simply to speak the language of markets more fluently than the Conservatives. It is to ensure markets serve society rather than dominate it”.

This all sounds reminiscent of this from March 2024: “Governments and policymakers are recognising that it is no longer enough, if it ever was, for the state to simply get out of the way, to leave markets to their own devices and correct the occasional negative externality”. That was Rachel Reeves in her pre-election Mais Lecture. Given her approach has been resoundingly rejected by her own voters, MPs and leader, it’s hard to see how doing even more of the same thing will rescue the economy. Better delivery always helps and there’s no doubt Burnham will arrive in post stuffed to the brim with political capital. But honeymoons are short when the champagne runs out and the hangover kicks in.

Burnham will be plagued from day one that he wasn’t even an MP elected on the party’s own manifesto. Hence the supposed allure of a snap election, as The Sun on Sunday reports is being wargamed. Whilst it would catch the ill-prepared Greens and Reform on the hop, it would also render half his colleagues redundant and surrender the numerical, if not actual, majority he will inherit. Labour will remain both government and opposition, whoever is sitting round the cabinet table.

But Burnham will not be without power. One of the first acts of his administration could be changing the mandate of the Bank of England. Louise Haigh hinted at this in her section of the latest policy paper produced by the Burnham-supporting Tribune Group. In “A new fiscal framework to renew Britain” she notes “As we approach the 30th anniversary of Gordon Brown giving the Bank operational independence to set interest rates, the time is right to re-examine the mandate and see whether better coordination and a greater focus on economic growth should also be included”.

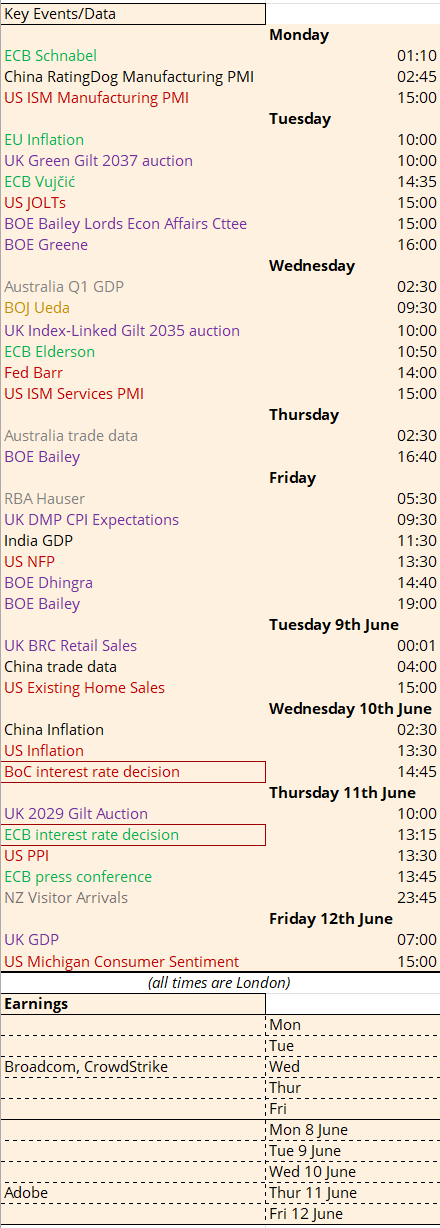

Governor Bailey can ponder that prospect during his upcoming fireside chat with one of the architects of Bank independence, Ed Balls, and Stephanie Flanders on Friday when he speaks at an event in Gordon Brown’s old constituency of Kirkcaldy to mark 250 years since Adam Smith wrote The Wealth of Nations. Before that, Bailey is in front of the House of Lords Economic Affairs Committee on Tuesday and giving a speech at the Investment Association Annual Conference on Thursday.

2. Inflation

Three months since the assassination of Ayatollah Khamenei and transit through the Strait of Hormuz remains elusive at best. Global oil stockpiles are reaching perilously low levels and ExxonMobil chiefs have warned it may be only a couple of weeks before inventory shortages become disruptive. Aluminium is facing a similar squeeze with Bloomberg calculating that “Combined stockpiles tracked by the LME, CME Group, and the Shanghai Futures Exchange would cover global supply for less than five days”.

In response, the US has been drawing down on the Strategic Petroleum Reserve and ramping up jet fuel production:

Meanwhile China has unexpectedly managed to reduce its imports without apparently tapping its SPR, which this useful report from the Oxford Institute for Energy Studies explains might be a result of refinery yield shifts.

But this can’t carry on forever. At some stage those demand and supply graphs force a new equilibrium. The bloodless economic state of “demand destruction” means that inevitably the oil price will have to rise. As Neil Chapman, the ExxonMobil SVP put it, “I think crude being in this sort of $90 to $110 for the last whatever it is, six weeks, has really been mitigated by running down inventories”… “we’re approaching unheard of inventory levels… once you get to that really low inventory level… a model would say Brent will shoot up… up to $150, $160”.

And so when we get the slew of inflation data in the next two weeks – Eurozone on Tuesday, US and China on Wednesday 10th June – that’s just the baseline from where we will be headed. The sudden recent turnaround from deflation to inflation in Chinese producer prices will permeate into consumer goods globally. Of more relevance to central banks will be the update on inflation expectations that we receive in the UK DMP CPI expectations on Friday and the US Michigan survey on Friday 12th June.

3. The ECB

We already know the ECB discussed interest rate hikes at their last meeting and therefore will finally deliver an increase on Thursday 11th June. Refreshingly, ECB Executive board member Isabel Schnabel acknowledged that even a foreign policy breakthrough does not offset the rippling economic shock, noting “Even if the war ended today, a lot of damage has already been done to energy infrastructure and global supply chains. So, even then, I believe that a monetary policy reaction would be needed”.

And it’s not just a case of whether energy prices are headed higher – time itself is doing the damage: “In terms of persistence, we have actually moved beyond the adverse scenario, which assumed a rapid normalisation of oil prices”. Inflation doesn’t need to accelerate to cause a knock on effect for inflation expectations and an adjustment in business and consumer behaviour.

4. The Fed

We will get an update on this in the context of the US economy with the bellwether releases of the Manufacturing ISM on Monday and Payrolls on Friday. The US consumer is already running down their savings to cushion the blow of higher prices. The personal savings rate is at its lowest level since just before the financial crisis:

And now there is a new sheriff in town. New Fed Chair Kevin Warsh can set an entirely new FOMC reaction function. The Fed has a dual mandate luxury that other central banks do not. Stagflation provides an excuse for putting the emphasis on the first syllable and overweighting the downside risk to growth versus the upside risk to inflation.

5. The BOJ

After the lost decades, Japan is finally experiencing some actual inflation, even before the Hormuz became blocked. It also has a fiscal stimulus in the pipeline after new PM Takaichi unveiled a $19bn package designed to subsidise fuel costs and tackle cost of living pressures. She has promised this won’t lead to increased debt issuance but inflation plus a weak currency and an energy price shock have taken Japanese bond yields to multi-decade highs.

Into this the Bank of Japan must look to tighten policy without frightening the JGB horses. Governor Ueda has been preparing the ground, telling the recent annual conference for the BOJ’s Institute for Monetary and Economic Studies “Japan’s experience shows that oil price shocks are never just oil price shocks. They are tests of the entire inflation regime”. He went on to sketch out prior oil price shocks, explaining that the impact depends on the prevailing conditions when they hit: “If inflation expectations are already high and wages are accelerating, the risk of second-round effects is large”.

He will emphasise this message at his speech on Wednesday at the flagship Kisaragi-Kai meeting. Akin to Jackson Hole, past BOJ Governors have used the speech to explain significant shifts in policy such as QE and YCC. Attendees come from the upper echelons of the Japanese political economy and as this one takes place two weeks before the pivotal BOJ meeting, Ueda will not pass up the opportunity to signal more hawkishness ahead.

6. Valuations

Where bonds must take account of the unstoppable force of a stagflationary shock, the equity markets are becoming an immovable object. If the dizzying ascent of stock markets feels disconnected from macroeconomic events, that’s because it is. Deutsche Bank have looked at the performance of the S&P500 in response to geopolitical shocks and noted that since the Iran War, it has flipped from being one of the worst performing to one of the best.

It might have something to do with the burgeoning arrival of one of the most highly valued companies in the world. On Friday 12th June we could well see the IPO of Elon Musk’s SpaceX which is expected to raise $75bn, valuing the company at a simply stratospheric $1.8 trillion. Of course it’s no longer simply a space company, pulling in cash from the successful Starlink satellite network – it is an AI company too, thanks to the acquisition of xAI. With AI having a famously voracious energy appetite, launching such a company into a global energy price shock might seem brave. But the economics of such shocks redistribute where and how products are made. And when a country’s political leadership is deliberately pursuing a policy of bifurcating supply chains, channelling scarce resources onshore and onto friendly allies, Musk’s bet might well pay off. To the victor the spoils.