The Two Weeks That Will Be (28th June 2026)

1. The UK

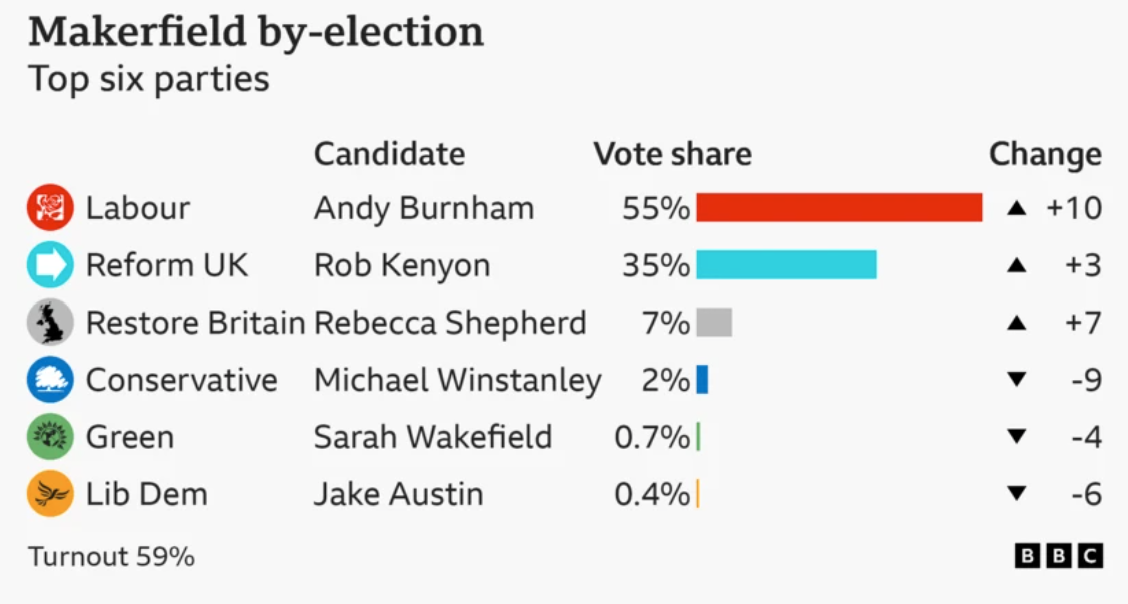

The Burnham Supremacy is assembling in the wings until PM Andy officially takes up the role on Monday 20th July. Three weeks ahead of that on Monday he will make a speech which will apparently outline his “economic vision“, or at least how devolution is a key part of that plan.

The rest of the fiscal plan will rest on the shoulders of Miliband, supported by Louise Haigh / Jim O’Neill / Andy Haldane and, most importantly, ex-OBR chief Richard Hughes. The signal is that the fiscal rules must be met but with some better work on behind-the-scenes engineering. Rather than HMT shouting at the OBR over its scoring, the new administration looks set to hoist the OBR with its own fiscal petard. They’ll argue for slightly different ways to interpret net debt, that productive investment can come from the public sector without crowding out the private sector, and even that there is a 10 year time horizon to meet an additional fiscal rule. Gaming the model will be harder but less acrimonious than arguing over the iterative output of the OBR’s spreadsheet.

It will still take the customary ten weeks for the OBR to prepare for the first Burnham budget, meaning the first opportunity to deliver one would come after conference season is over and parliament returns in the week of 12th October. Until then the UK must once again sit and endure endless lobbying and speculation.

2. Inflation

With the oil price plummeting on the US/Iran ceasefire and the return, albeit small, of ships transiting through the Strait of Hormuz, it’s as if the inflationary impact of the last three months were some sort of fever dream. The latest inflation print from the Eurozone is released on Wednesday and for China on Thursday 9th July.

Except the dislocation isn’t over. Fertiliser prices might have plummeted (Middle East urea prices have halved) but that’s because farmers couldn’t afford it and demand has dropped. The knock-on impact will only show up in the harvest, where some crops have been prioritised over others. Then if supply of certain crops falls but demand remains the same, the price of the harvested food will go up. We are still in the midst of the chop of economics, where demand and supply meet many interim equlibria before attaining their final resting point.

The Middle East is not going to be used in the same way again. Japan has already adjusted its naphtha imports: in April, those from the Middle East fell by 89% from the prior year and those from the US rose six fold.

The first estimate of the number of ships stuck in the Strait of Hormuz is 1,200, carrying $125bn worth of goods. That is like having 1,200 Ever Givens – which had 450 ships stuck behind it after just six days in the Suez Canal in March 2021. It took four months to get back to normal after that episode. It is unlikely Hormuz will ever be the same again.

3. Financial Stability

Not that this seems to bother financial markets. “Don’t Get Caught Short” is the mantra of the markets since Liberation Day, meaning the status quo is always to be long, and longer than you might want, just in case someone pays you out of your position. But every so often reality peeks through. Hence the blockbuster results for chip-maker Micron Technology introduced a cautionary note as the market had to re-rate higher the sheer cost of hyperscaler capex. Apple and Microsoft belatedly raised the price of their core products. The inflation that has supposedly disappeared thanks to Trump and the IRGC signing a deal-that-opens-the-path-to-a-deal is far from in the rearview mirror. And once one technology stock tumbles, so do the rest.

Then there is the contagion to those who play “Don’t Get Caught Short” by being levered long. The KOSPI has doubled in value this year alone. SoftBank is becoming a high-beta OpenAI play ahead of the latter’s (now delayed) IPO. Both now take a battering when the AI train wobbles – but also rally back hard when the bulls buy the dip.

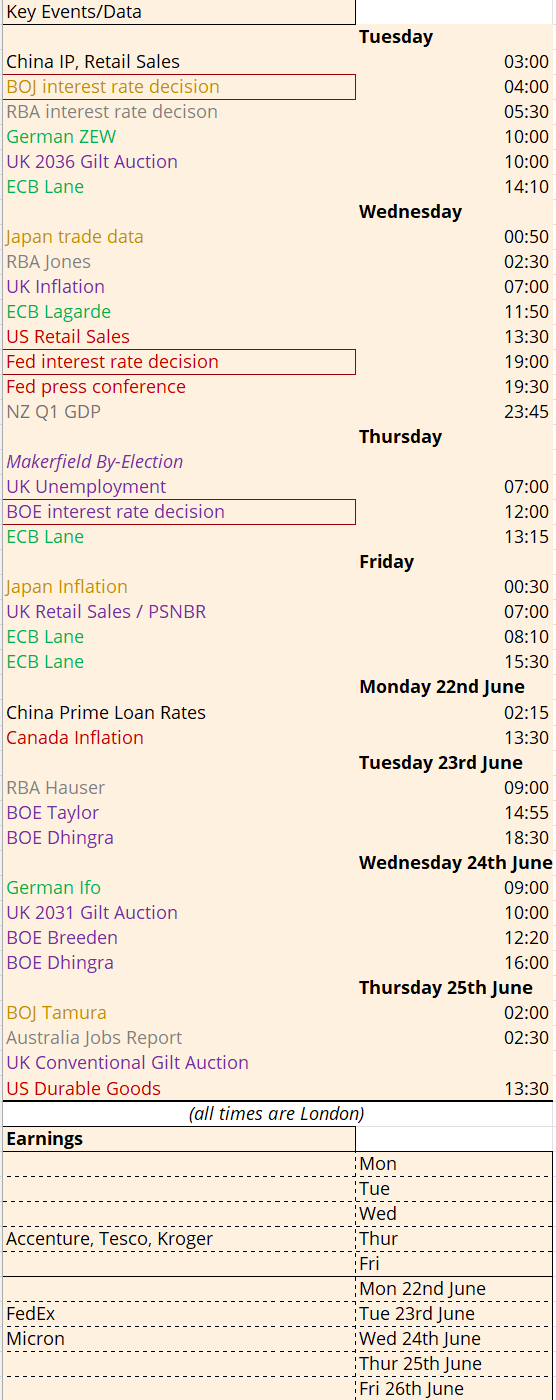

All of this suggests there is a structural issue lurking. The latest BIS Annual Report has sounded the alarm, warning of four “pressure points that demand urgent attention” which could combine to create contagion across markets: inflation; “unsustainable” AI capex; “exuberant risk appetite”; and high public debt levels. The Bank of England produce their latest financial stability report on Tuesday 7th July. We are now into quarter and half year end. Rebalancing flows could take some of the froth out of the market, helping to de-leverage safely.

4. Central Banks

Such topics will be on the agenda at next week’s annual ECB conference at Sintra. On Wednesday we will hear from a panel of the Fed’s Warsh, the ECB’s Lagarde, the BOE’s Bailey and Bank of Canada’s Macklem. On Thursday we get the unusually timed US Non Farm Payrolls release. Given Warsh has signalled the market must get used to making its own mind up on data, rather than being spoon fed forward guidance by the central bank, he is likely to sit back and enjoy his time in Portugal.