The Two Weeks That Will Be (6th April 2026)

We can’t be as confident as Chance the Gardener that there will be growth in the spring. If anything, the passage of approximately 150 ships through the Strait of Hormuz during the whole of the last month compared to the pre-war average of 150 per day is making a recession ever more likely. Five years ago, one ship got stuck in the Suez Canal for six days. The Ever Given dominated the news for a locked-down world, spewing forth memes as people feared delays to their Amazon packages. With around 450 ships stuck behind it, the backlog took five days to clear, with normal conditions only fully returning a couple of months later.

The current state of affairs is orders of magnitude worse. We now have the equivalent of something like 3,000 Ever Givens stuck. All are stuffed with the rather more important cargo of barrels of oil, flammable LNG, and precious fertiliser ingredients. The situation is summarised in the picture below by @VolaTim:

Whatever happens from this point forward, this is where we are right now. And so the most useful data to monitor will be that which is most timely. Everything else is already out of date.

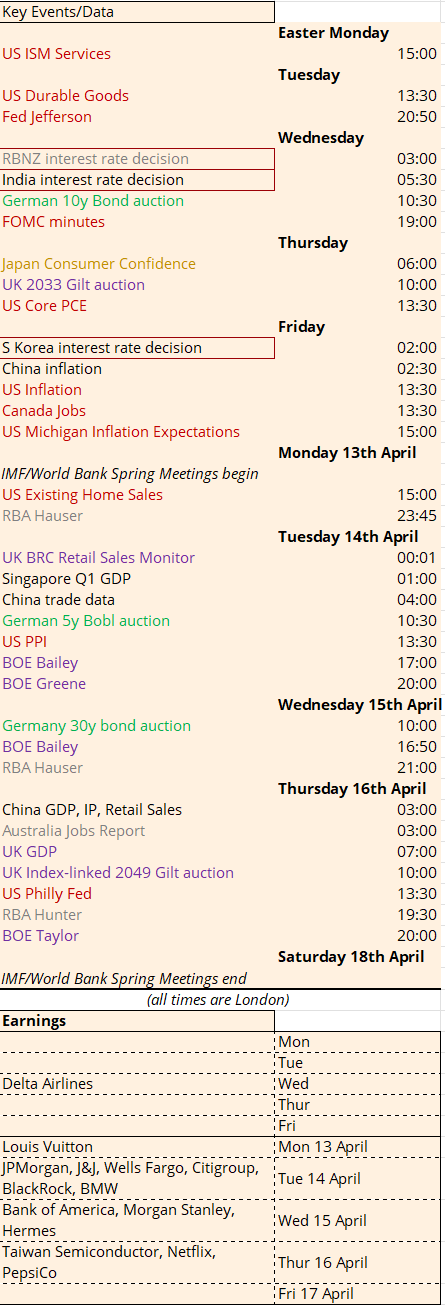

Step forward Japan Consumer Confidence on Thursday, UK BRC Retail Sales and Singapore Q1 GDP on Tuesday 14th April, US Philly Fed on Thursday 16th April and – even more than US inflation at 13:30 BST on Friday – the US Michigan Inflation Expectations released 90 minutes later on Friday.

And it’s inflation expectations that are firmly in the sights of the world’s central banks as they face a shock that, even with all the surrounding uncertainty over its duration, is already known to be inflationary. On Wednesday we get interest rate decisions from New Zealand and India, followed by South Korea on Friday. These are all nations that are some of the hardest hit by the shortages from the Middle East due to their dependency on energy imports.

We also get earnings updates from some of the most impacted businesses. Delta Airlines report on Wednesday. If we think shipping tankers will be wildly out of sync from their normal schedules then pity the airlines. Not only facing the random and repeated closure of airspace, they must also deal with the challenge of not knowing if they can fill up with jet fuel for their return journeys. The entire sector is in a state of flux. Qatar Airways has parked 20 of its planes at the lesser-known Teruel airport in Spain (last in the headlines during the Covid pandemic when over 130 planes were stored there). Etihad has just cut fares by half for May and June – you can get business class from London to Sydney for just under £2,500. You have to travel via Abu Dhabi of course. If you prefer slightly less risk of incoming missiles by going via Singapore with BA, you’re looking at a price four times higher. With threat comes opportunity. Cathay Pacific has announced additional capacity for flights to Europe.

Will the usual luminaries find this affects their travel to the IMF/World Bank Spring Meetings from Monday 13th-Saturday 18th April? Zoom could find itself once again in vogue. In any event, the IMF and World Bank have already issued a joint statement with the International Energy Agency to announce “a coordination group… to monitor developments, align analysis, and coordinate support to policymakers to navigate this crisis“. They highlight that “This is especially the case for countries that are most exposed to the downstream impacts from the war and those confronting more limited policy space and higher levels of debt“. This sounds like – sensibly – a plan for prioritisation given limited resources. Triage has already begun.

With lower growth and higher inflation meeting huge piles of debt, government bond auctions pose a risk. With the UK continuing to hold the role of high-beta player whether bonds are rallying or selling off, we will be keeping an eye on the 2033 Gilt auction on Thursday and the 2049 index-linked on the following Thursday 16th April. If something goes awry at the usually solid German auctions on Wednesday (10y), Tuesday 14th April (5y) or Wednesday 15th April (30y) then that would send chills through other more highly indebted nations.