From Barrels to Bonds to Breakdown

++ The physical fiscal cascade has begun. We are in a supply shortage that no protagonist can solve and that the belligerents are incentivised to maintain, if not exacerbate. Stimulative monetary and fiscal intervention is not only useless but counterproductive in such a stagflationary shock, even as electorates will demand action. Bond markets and voters are set for an explosive showdown as governments with weak mandates inevitably fail to please either. ++

- Physical Shortages

The Ever Given became stuck in the Suez Canal five years ago for six days. There were 450 ships queued up behind it, taking several days to clear and several weeks to return to normal. The current blockage in the Strait of Hormuz is like 800 Ever Givens (as per estimates of stranded vessels by Lloyd’s List).

But these vessels have been stranded for several weeks. Some of their cargo has weathered, for example LNG evaporates at a daily rate of ~0.1%. Other ships have then been forced onto longer journeys, often re-routed to the highest bidder for their precious cargo. Some ships can’t transit certain routes due to their dimensions. Round Hormuz pegs won’t fit in square Malacca holes.

Japan has proudly announced that by May it expects more than half of its oil imports to come from routes that do not include the Strait of Hormuz, potentially including Brazil, Nigeria, Azerbaijan and Malaysia. If their output is going to Japan then it’s not going to its usual destination. Ramping up production to meet extra demand can’t be done at the flick of a switch, given physical constraints on wells, transport and labour. All of this disrupts the usual flow of tankers around the world, adding cost and time to journeys.

Beyond the stranded tankers, there is actual damage to infrastructure. QatarEnergy said damage to its LNG facilities in Ras Laffan will take three to five years to restore. The Khurais onshore complex in Saudi Arabia is still undergoing repairs for its 300,000 barrel a day outage.

This is reminiscent of the global dash to secure oxygen during COVID, or how letters of credit for trade finance froze once Lehman collapsed. If the supply isn’t there, it isn’t there.

- The Cascade

And the supply of one essential ingredient has a knock on effect to whatever it is used for.

Helium is essential to semiconductor manufacturing as its low boiling point enables efficient cooling of equipment, preventing overheating during intricate fabrication steps. About a third of the world’s helium supply comes through the Strait of Hormuz.

Fertiliser requires various components currently sitting on those stranded tankers in the gulf such as urea and ammonia, along with feedstocks like phosphate and sulphur. With fertiliser failing to arrive during April, it cannot be fully disseminated by planting season in June, resulting in the potential for exponentially depleted harvests in September.

Then there is the knock on effect on transport. Petrol and diesel shortages hamper the workers trying to reach logistical hubs. Fears of such shortages create their own self-reinforcing logic. Queues have been reported in Kenya, India, Australia amongst others.

The spike in jet fuel prices and domestic hoarding means airlines face the challenge of scheduling without knowing if they will be able to refuel for the return journey. China and Thailand have halted jet fuel exports; Pakistan pilots are carrying maximum fuel from abroad; AirAsia X is loading extra fuel in Malaysia before flying to Vietnam due to limited supplies. If everybody tries to insure themselves with precautionary extra fuel, the problem gets worse.

Airspace restrictions have compounded the problem. Teruel airport in rural Spain, usually used for routine maintenance, currently serves as a parking lot for 20 Qatar Airways planes. In the depths of the pandemic, around 140 planes were parked there. Challenge also brings opportunity – with Chinese airlines able to fly over Russian airspace, Cathay has been adding extra capacity to Europe.

- Bond re-pricing

Although Asia and Africa are particularly vulnerable to the supply shortages, this is not just a regional issue. In a highly globalised world, competition for scarce resources can only ever result in one outcome for all: higher inflation. China just recorded positive producer price inflation for the first time in three and a half years.

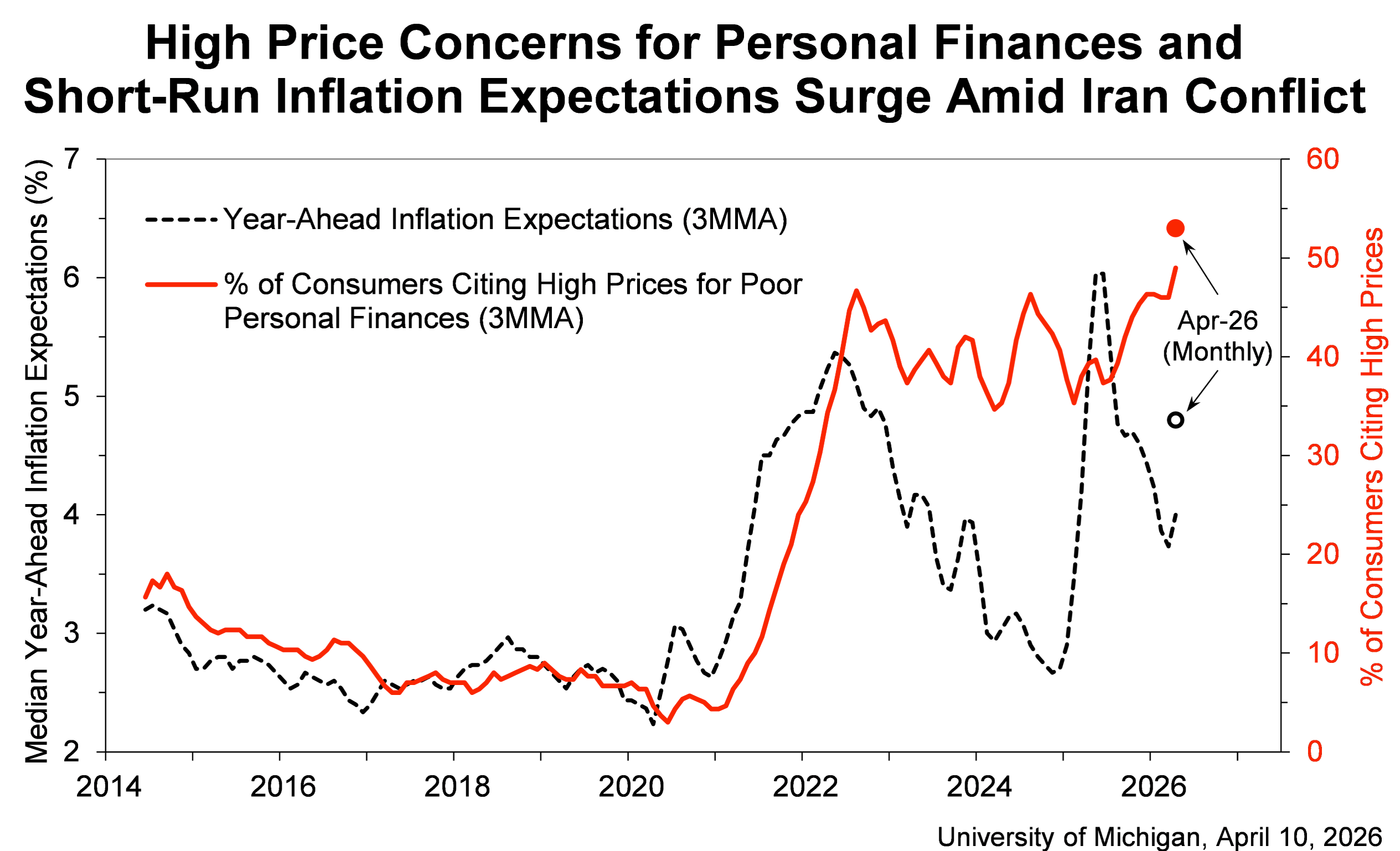

Chinese PPI is usually a leading indicator for the direction of US CPI. And it’s not current inflation that perturbs the world’s central banks but instead the effect on inflation expectations, particularly having been caught slow off the mark following the Ukraine war. Consumers remember. In the UK, the YouGov Citi survey of short-term inflation expectations jumped to 5.4% from 3.3% the prior month, hitting the highest level since inflation itself was above 10%. The latest US Michigan Consumer Sentiment survey showed year-ahead inflation expectations spiked to 4.8% from 3.8%, the largest one month increase since April 2025:

As the chart above shows, the concern over high prices impacting people’s personal finances (the red line) never ebbed away after the 2022 shock. This hysteresis is precisely what central banks hope to quash by a hawkish pivot.

We are no longer in the disinflation debt-bust world that many experienced after the financial crisis. Brexit began the process of reconsidering supply chains; the pandemic made it global; and geopolitical defence concerns under a radical US administration seeking to redraw its place in the world have now made it everyone’s problem. This is a world of 2-4% inflation rather than the 0-2% that we had become used to during the NICE decade and the subsequent QE decade.

Stagflation would tend to create an inverted yield curve as short term higher central bank rates are offset by expectations of lower growth and safe haven demand. But not if long-term debt is risky due to a lack of fiscal credibility. Significant budget deficits and high inflation without any growth can combine to make fiscal kryptonite, creating a fiscal crisis if a government fails to put its house in order as its position declines.

- Financial Markets

Rising risk premia in government bond markets will permeate through all financial assets. If currencies come under pressure, exacerbating inflation and prompting an even greater central bank response, the reaction could be violent.

We were already in a world where valuations of the euphoric technology sector had come into question. AI and data centres could not be a sector more dependent on expectations of cheap and plentiful energy supply alongside manageably low interest rates for the huge debt issuance required for large scale capital expenditure. Private credit has rested on similar laurels.

Volatility will remain raised as the scale and speed of the physical shortage becomes apparent. We had already flagged up the 25 level in the VIX as an inflection point, below which benign outcomes are overweighted and above which all the negative unpriced risk floods into valuations. Liquidations have already begun. Everyone’s darling, Gold, already suffered its largest one day drop since 1983, even before the Iran crisis began. Redemption requests have had to be capped at private credit funds from BlackRock, Blackstone, Apollo, KKR, Carlyle, Morgan Stanley, Barings, and everyone’s canary in the coalmine, BlueOwl. Banks will not be immune from the discovery of cockroaches, as we have seen recently with the potential losses for Barclays, Santander and Jefferies from the collapse of Market Financial Solutions Ltd.

The Bank of England Financial Policy Committee’s latest report warned “Heightened uncertainty and unpredictability have made it harder for markets to price underlying economic fundamentals, increasing the likelihood and magnitude of sharp market shifts in response to new information… These conditions increase the potential for several vulnerabilities to crystallise simultaneously, underscoring the importance of timely and active risk management by market participants”.

- New World Order

But this is not a story of financial markets. We are in the heart of a battle for the future of the global political system. As US Treasury Secretary Scott Bessent put it in the every first sentence of his op-ed for The Economist in October 2024, “The United States must play a more active role in reshaping the international economic order”. He concluded “Clearer segmentation of the international economy would provide more effective levers to confront the underlying sources of imbalances than the currently dominant bilateral approach. Additionally, the cost to remaining outside the perimeter would be high. Without access to US markets, Chinese overcapacity would instead threaten the viability of other countries’ domestic output. And would-be hegemons outside the US-led zone are unlikely to prove as benevolent as the United States in the post-war era”.

The cost is precisely what the US administration need for the nations to decide on whose side they choose to take. Even Jamie Dimon has said of the Iranian conflict, “It’s much more important that this be successfully completed than what the market does”.

Iran might judge it has little left to lose and a relatively low cost chokehold via the geography of the Strait of Hormuz. Therefore the two belligerents are not incentivised to de-escalate. Even if they did, the supply shock would persist even if shipping were restored immediately.

- Political impact

Everyone else must pick up the pieces. Another cost of living shock will be politically painful but the impact will vary depending on the strength of the government. A country with a popular leader with a strong mandate and low energy costs will weather the storm better than the reverse. Japan, Australia and Canada have recently had elections that delivered their leaders a popular mandate with political capital to burn. But that doesn’t mean it will be easy. Japan recently passed its largest ever annual budget but only after the chair of the upper house budget committee provided a casting vote, the first time a tie had happened since 1980. Australian PM Albanese has been on a whistle stop tour to Singapore, Brunei and Malaysia as he attempts to shore up fuel supplies following criticism he was slow off the mark to respond.

France, Germany and the UK are struggling with weak and unpopular leaders who barely have a mandate for most of the action they’ve taken to date. Where the UK faces both high energy costs and high debt, France still has nuclear power whilst Germany still has room for increased debt issuance.

- The UK

Cometh the hour, cometh the lawyer with little instinct for politics, shorn of the adviser who took him to victory, constrained fiscally and nursing a third place electoral loss in his party’s heartlands. The UK’s prime minister is almost uniquely placed for his vulnerability. U-turn after u-turn has undermined fiscal credibility, increased labour costs have proved inflationary and net zero has embedded higher energy costs. Even the gutted welfare reforms, which were only going to restrain the growth in welfare spending rather than reduce it, saw 47 Labour MPs rebel.

The Labour Party will rue the day they failed to replace their leader for someone, indeed anyone, who could deliver political salesmanship and, more importantly, party discipline. The government has plummeted in the polls, seeing the 34% it won at the election more than halve to 16%, and there hasn’t even been an actual economic shock yet.

Until now.

Legal opinions on the use of air bases and saying you’re “fed up” with “the actions of Putin and Trump” putting up energy bills will not pass muster for families who can’t fill up the family car with petrol or farmers unable to access red diesel. Not just it being expensive to do so – but not being able to do so at all. Ditto if the family holiday to the Mediterranean is cancelled because flights are cut. To govern is to choose, not to complain.

And there are few choices left available to an ideologically damaged Labour party. When Hannah Spencer, the new Green MP for Gorton & Denton, made her victory speech at the count, Labour grandee David Blunkett said he was left thinking “What is that has driven this young woman to join the Greens rather than Labour?”. She had said “working hard used to get you something. It got you a house, a nice life, holidays, it got you somewhere. But now, working hard, what does that get you? Because talk to anyone here and they will tell you, the people work hard but can’t put food on the table, can’t get their kids school uniforms, can’t put their heating on, can’t live off the pension they worked hard to save for, can’t even begin to dream about ever having a holiday, ever. Because life has changed. Instead of working for a nice life, we’re working to line the pockets of billionaires. We are being bled dry”.

Step forward a new inflationary shock that will only exacerbate her sentiment.

And to add insult to injury, the fiscal position means the Labour Party can’t even deliver the scale of the help promised by Liz Truss (and then, in smaller terms, by Jeremy Hunt) in the wake of the Ukraine inflation spike. The Debt Management Office estimates Gilt sales this fiscal year of £252bn – that’s almost half as much again as were sold under Jeremy Hunt in 2022-23 when Gilt sales were £170bn.

Some extra stimulus might be swallowed if there were sort of concomitant reduction in government spending. But given Labour MPs rebelled over an attempt to rein in welfare spending, it is impossible that they would support an actual reduction in spending. It would only take 33 more MPs to join those welfare rebels and the government’s majority is lost.

In an attempt to avoid such a confrontation, Rachel Reeves has been signalling any help will be very carefully targeted. This leads to the possibility that only those in receipt of benefits will receive support with energy bills, which would hardly defeat the Hannah Spencer argument that “working hard, what does that get you?”.

Any long-term plans risk being blown out of the water by events. Fuel shortages are toxic. Even Tony Blair saw his double digit poll lead eradicated in September 2000 during the petrol protests. Sitting quietly and hoping problems go away isn’t usually a winning strategy for a government. Starmer has shown he is not exactly fleet of foot, pressing ahead with a new fiscal year media speech on the measures taken to address the cost of living, just as a huge new cost of living shock hoved into view. He was also on a family holiday in Valencia in the days leading up to Trump’s deadlines with Iran. Whilst politicians are people too, it might not have been the most judicious moment to be out of the country.

There is already alternative leadership in position. Secretary of State for Energy Security and Net Zero, Ed Miliband has graced the front cover of the New Statesman under the headline “How did Labour’s former leader become the most powerful man in government?”. The Spectator reported that it was Miliband who led Cabinet opposition to US military action in Iran at a National Security Council meeting the day before strikes began. Starmer told parliament that decisions over oil and gas licences at the Jackdaw and Rosebank fields lay with the energy secretary, in one of his most remarkable letter-of-the-law applications of delegation so far. The Prime Minister might be in office but Ed Miliband is in power. This could be formalised following the anticipated electoral defeats at the local, Welsh and Scottish elections on 7th May. A reshuffle would be a cost-free way for the PM to look like he’s regaining the initiative and promoting Miliband to Chancellor would confirm the left is back in charge of the party.

All of which leaves us with the battle royale ahead: Miliband vs the Market. As Gilt yields ratchet higher and pressure for fiscal consolidation increases, Milibandism will double down in the opposite direction.